Portfolio Spotlight: Macfarlane Group PLC

10-Year EPS CAGR of 11.2%, while paying 2-3% dividend. All yours for 12x LTM P/E

Macfarlane is essentially a roll-up in the packaging distribution sector. The algorithm is that they generate ~20% returns on capital, dividend a quarter of FCF and invest the rest in consolidating this fragmented sector.

That sounds pretty good to me, but the stock price chart for the last 5 years does not look impressive at all: from 94p then to 124p now. It did pay an annual 2-3% dividend though.

But under the hood, the fundamentals kept humming along. Yep, another case of multiple contraction.

I like setups like this. The stock chart looks boring and uninteresting, but the company has kept executing. Coiled spring comes to mind, although I hate that term.

I don’t have many original insights on this name, so in this post I’ll mostly be quoting highlights from other write-ups. They will be linked down below.

Company Introduction

Macfarlane is a distributor (89% by sales) and manufacturer (11%) of protective packaging with 38 locations in the UK, with one location in each of Ireland, Netherlands, and Germany (all leased). Specialized packaging for e-commerce has grown in recent years to reach 26% of 2022 sales, but Macfarlane’s bread-and-butter remains custom-made packaging for industrial goods.

This is one of those great little niches where you’re selling something that’s only a small percentage of your customers’ costs, but if something goes wrong, the cost to your customer becomes really large.

It’s boring and resilient: offering consistent, predictable earnings stream across economic cycles.

Unloved Compounder

I really like this article from April 2023 in which the author compares MACF with select UK industrial/distribution compounders. It really drives home the point that Macfarlane seems cheap for no apparent reason.

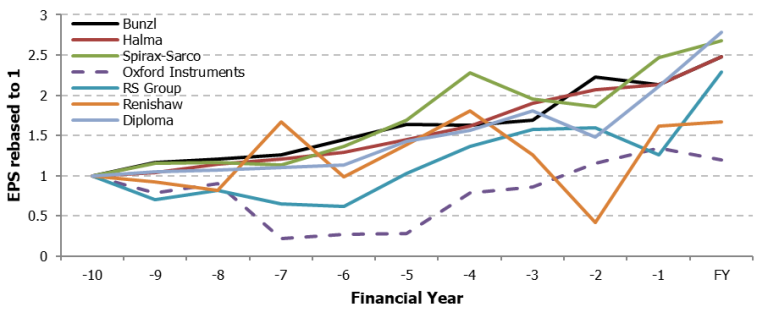

The article starts with an EPS growth chart for some “classic” UK compounders: Bunzl, Halma, Spirax-Sarco, Oxford Instruments, RS Group, Renishaw and Diploma.

People are drawn to businesses like these because the numbers match their pre-conceptions. They think “scientific instruments must be a good business”, and the numbers bear it out. They consider that “distributing small, mission critical products must make for quite a reliable profit base”, and the figures chime.

Macfarlane has actually outperformed all of them in EPS growth!

Macfarlane sells packaging. The entire market grows or shrinks by a low single digit percentage point amount each year. It is irreplaceable and intrinsically tied to every factor of the physical economy. Macfarlane is the largest independent distributor of packaging in the UK.

I think Macfarlane looks a lot like the businesses I highlighted earlier. In some ways it is worse; return on capital and margin is slightly lower, as shifting packaging around is inherently a more competitive business than (for instance) producing scientific instruments. In some ways it is better; packaging is about as non-cyclical as it gets, and revenue and demand is very easy to forecast, with little lumpiness and no customer concentration.

ESG = Headwind?

One bear case that gets brought up sometimes, is ESG:

The ESG-trend towards less packaging - or at least less harmful packaging - is actually a boon to the business, with Macfarlane serving in a consultant-like role to help customers meet ESG goals such as engineering reduced plastic in the containers.

Valuation

At the current price of 124p, Macfarlane trades at a market cap of £199m and an EV of £239m. This implies a LTM P/E of 12x and a NTM P/E of 10.5x. That’s just too low for a quality business like this.

On top of that, the LTM Net Debt/EBITDA is 1.1x, which is arguably underlevered for such a steady earnings stream. This provides flexibility on the balance sheet benefiting either the company itself or a potential acquirer.

Why does the opportunity exist?

In general UK small caps are simply unloved. Additionally, a significant institutional investor reduced or has been reducing their stake in Macfarlane since the previous year.

Macfarlane is a longstanding holding which the manager intends to retain within the portfolio, although it expects to a smaller weighting over time.

Some companies embrace their cheapness and take advantage of it with share buybacks. Macfarlane however seems to prefer M&A. That is totally acceptable if it yields comparable returns. However, this doesn't directly address the issue of a low share price. Instead, Macfarlane focuses on business growth, creating value that way and eventually the share price will reflect this progress… right?

But in the meantime, you just get to hold a solid business reinvesting earnings at attractive rates of return, while paying a modest dividend.

Resources

Write-ups from which I quoted:

Older write-up: Ticking all the Boxes (October 2021)

Twitter accounts to follow on the name: mainly just Lewis Robinson, who also happens to be the author of 2 articles linked above.

Disclaimer: This content is for educational and entertainment purposes only and is not intended as financial advice. Perform your own research and consult a qualified financial advisor. The author may hold positions in the discussed stocks. This is not a recommendation to buy or sell securities.

Love the short-and-to-the-point format of your posts! Important points only.