Q1 2025 Portfolio Review

Flat YTD vs -8.7% for S&P 500 in EUR

Writing this Q1 update in mid-April feels strange… this month’s been such a rollercoaster, it’s hard to remember what even happened in Q1.

So I’m keeping this one short and focused strictly on Q1. Just pretend it’s April 1st and this hit your inbox right on time.

I. Results

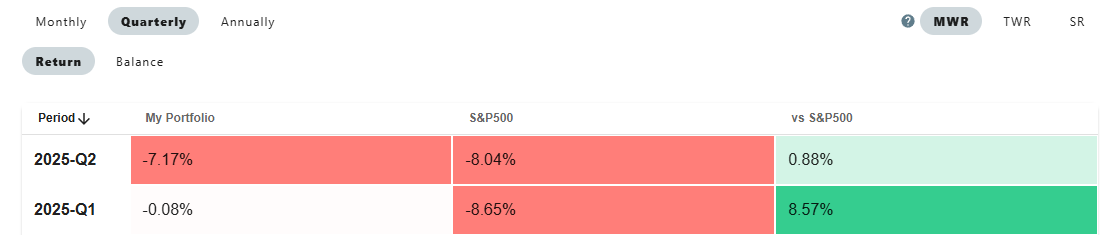

Q1 2025 Returns

No Deep Dives Portfolio: -0.13%

S&P 500 (in EUR): -8.69%

Portfolio on April 1st, 2025

After underperforming the brutal post-Trump election rally (which I covered in the previous quartery letter) the portfolio finally got its chance to strike back in Q1.

Last year I wrote, somewhat dramatically:

The cross you bear as a value investor as that you sell before the top, and because of that you’ll often underperform in times of extreme greed. However, I hope to make up for that in other periods.

Meager returns in the first quarter, but it does look like we’ve at least made up for the Q4 2024 underperformance.

II. General Themes & Thoughts

Trump’s break with traditional allies has been so forceful it’s lit a fire under the EU: both in the form of increased defense spending and a German fiscal shakeup that includes a €500n infrastructure investment fund.

The broader vibe feels like the end of American exceptionalism. I know, nothing ever happens... but this time does feel different. From consumer boycotts of U.S. products to global allocators rethinking their overweight to U.S. equities, the shift is noticeable. And it could snowball: outperformance attracts flows, which fuels more outperformance. What if being overweight U.S. stops being the default?

That said, I’m not making explicit portfolio bets on an “EU resurgence.” But if I already like a stock and it stands to benefit, then this can be a nice cherry on top.

On the other hand:

III. Portfolio Updates

Exited Positions

Sold Verallia at €24.08

Trimmed PM 0.00%↑ at $153

Sold CZR 0.00%↑ at $34.25

Sold GCO.MC at €49.5

As always, transactions are posted & briefly discussed on Substack Notes.

New Positions

Bought Greggs (GRG.L) at 2133p: compounder in temporary dip. Unfortunately the dip kept on dipping

Added to Barry Callebaut (BARN.SW) at 1044 CHF: compounder in temporary dip. Unfortunately the dip kept on dipping

Bought SECURE Waste Infrastructure (SES.TO) at C$ 14.36

Bought Kitwave (KITW.L) at 250p

Added to Inchcape (INCH.L) at 702p

Top Contributors

Millicom ( TIGO 0.36%↑ ): +16.4%

In January, Millicom finally announced their shareholder remuneration policy. The biggest eye catcher was the intention to pay a regular dividend, to be sustained or grown, starting at $3 annually. That was a 12% dividend yield on a stock price of $25 at the time of announcement.

Sounds suspicious right? How can a company just start paying a 12% dividend?

The answer is simple: Millicom has transformed into a cash printing machine. They generated $725M of FCF in 2024, with more expected the coming years. The declared dividend would be about $500M per year, so easily covered by annual FCF.

They’re also working on a major M&A deal in Colombia, which could reshape the market and push FCF north of $1B in a few years. If it doesn’t happen, they’ll have $1B to deploy in 2025 regardless.

As always, I’ll refer you to

for more background info:Philip Morris ( PM 0.00%↑ ): +25.6%

Good results with Zyn on fire: improved EPS forecasts and some multiple expansion have catapulted this stock to over $157. I bought this for $100 at 15.3x fwd P/E and we’re now at 22.2x. This does make me a bit uneasy, as a “value investor”, so I trimmed part of the position while holding onto the rest.

Sigmaroc (SCR.L) +24%

SigmaRoc is the leading EU aggregates/limestone operator that transformed itself by acquiring the European assets from CRH. It’s listed in the UK, but basically all about Europe with broad exposure to construction and industrial markets.

It’s well positioned to benefit from Germany’s infrastructure “bazooka,” which has already sent ripples through the market. Even after the recent rally, it’s still trading at just 10x forward P/E and estimates likely still need to catch up.

Chemring (CHG.L): +13.5%

I bought Chemring partly as a play on rising EU defense spending. But unlike something like Rheinmetall, it’s not a clean pure play. For example, there's been chatter that the EU prefers this new spending to stay within the EU, without the UK.

Interestingly, the company reportedly received take-private interest before the Zelensky/Trump Oval Office moment that reignited the EU defense theme. But if protectionism ramps up, will a U.S. firm even be allowed to acquire a UK defense contractor?

Grupo Catalana Occidente (GCO.MC): +35%

Last quarter, this was still one of the top detractors. But by the end of Q1, it received a take-private offer from the controlling family at €50 per share, when it was trading at €42.

A meager premium and the stock is still cheap. A case could be made that the family might be pressured to raise the offer.

But that’s a different setup with new risk/reward. I sold my shares at €49.5, happily passing on the merger arb trade, which now looks like:

Small upside if the deal closes

More upside if the offer is raised

Downside if the deal collapses and the stock drops

Some investors get attached to “their shares” and don’t want to insiders to “steal the company”. I get that, but in the end it’s just about the risk/reward at the current stock price (although taxes can complicate things). At €49.5, I was quite happy to move on to the next one.

Top Detractors

Mattr (MATR.TO), Winpak (WPK.TO) and Linamar (LNR.TO) all got hit by some Trump tariffs uncertainty, and were down 15-20% as a consequence. In addition to that, MATR quickly went from fintwit darling to an oversold outcast.

Google got swept up in the broader U.S. tech selloff, and it looks like I was a bit early on the Greggs dip: shares took another hit after the latest earnings update.

IV. Closing Thoughts

I didn’t cover every stock as in depth as I wanted to. But I’d rather get this out now than wait, only to have a few more weeks of DJT headlines wipe out any memory of Q1 2025.

April’s been brutal so far, and the dollar’s devaluation has added extra sting for international investors. In euro terms, the S&P 500 is down 16% YTD.

That said, the portfolio is still outperforming. You can’t eat relative performance, but it I don’t think I can ask for much more than this right now.

What's your take on SES.TO cyclicality? In 2015, O&G production in CA got blasted and all their segments got stomped.

No me robes mi catalana occidente!!!!! I don't mind selling stuff with a premium, its just that its a long term compounder and we have to pay taxes and stop the compounding