Q4 2025 Portfolio Review

Up 7.56% in Q4 25, +30.97% in FY25

I. Results

Q4 2025 Returns

No Deep Dives Portfolio: +7.56%

S&P 500 (in EUR): 2.63%

Really happy with the performance, especially when compared to the index returns.

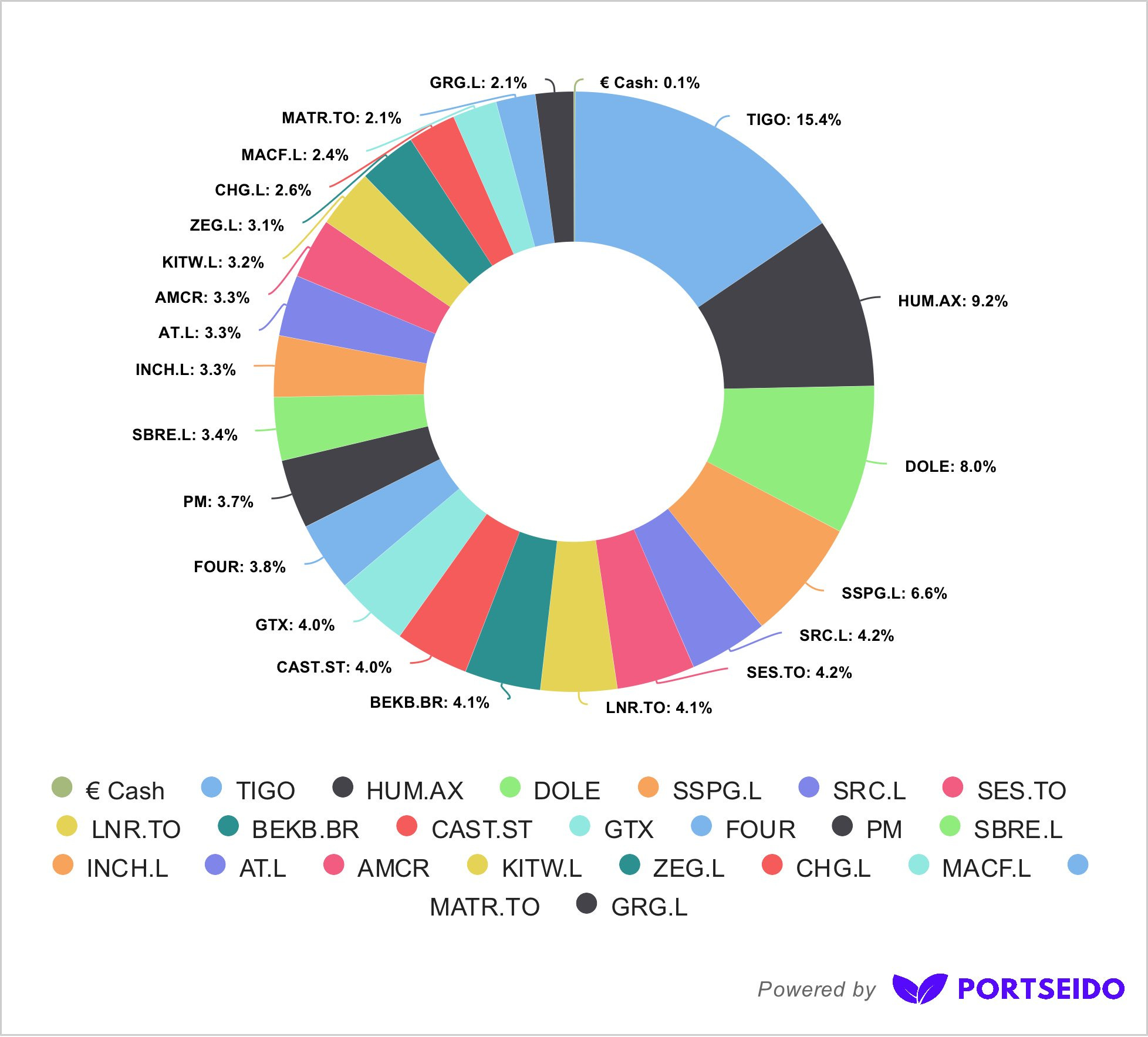

Portfolio on December 31th, 2025

II. Portfolio Updates

New Positions

Initiated a position in DOLE at $13.22, 5.1% of portfolio and added more later in de Q. The post below explains the special situation setup at DOLE, but also the long term appeal. There was no quick bounce as the author hoped, but I think we still have the opportunity to be a decent business at an excellent price, with potential catalysts on the horizon.

Dole reported in-line Q3 2025 results, issued slight guidance upgrades, and announced the buyback authorization we were looking for.

Bought Castellum at 106.9 SEK:

Castellum is giving me strong TIGO vibes, even though the companies are unrelated. A lot of traumatized investors no longer want to look at the stock, which is often the setup for opportunity. A new large owner with a proven track record in the sector (Akelius) stepped in opportunistically, built a meaningful stake, and put his own people in charge to reset the business.

Castellum is a Swedish real estate stock, and that entire space has been painful. The company had to do a rights issue in 2023 to repair the balance sheet after the previous CEO and large holder was margin called. Akelius then emerged as the largest shareholder. In July 2025 he installed his candidate as chair of the board, and at the end of August selected a new CEO.We just got the first earnings report under the new CEO, and my immediate reaction was that this CEO gets it. “The mission from the owners and BoD is crystal clear: Castellum needs to be more profitable. That’s exciting and fun, but won’t be a walk in the park. Heyday of RE is over, it’s back to basics. Rates are not 0 anymore. It’s turning over every stone to be more (cost) efficient.”

He talked about “more entrepreneurship, less bureaucracy,” and about the need to “make sure we own the right properties in the right locations (this can mean both buying and selling!).” Importantly, he said the “property portfolio is better than I thought: locations are good, right location for right purpose. In better condition than expected,” and was clearly “all in favor of buybacks at the current stock price and HUGE discount to NAV.”

That said, the turnaround is not here yet. The focus is stabilization first, and management was explicit that it “may get worse first before it gets better again.” The dividend may be cut to prioritize compounding NAV per share. I like that mindset, even if parts of the investor base may not.

Bought SSPG.L at 148p (5% position). Immediately got rewarded with a good earnings report.

Bought AT.L at 311p (3.5%): Provides rental and services for subsea construction, inspection, repair, and decommissioning. Trading at a forward P/E of 7x, well below historical levels. It's cheap on current earnings, widely disliked, yet earnings are expected to grow. The market likely wants to see confirmed organic growth before rerating.

Bought $FOUR at $67.41: Payments sector is out of favor. FOUR has messy accounting and a history of acquisitions, but it’s growing and appears to be executing well. Shares have rerated with the broader sector.

As scuttleblurb said:

“Despite Shift4 performing more or less as expected, its stock has lost more than 30% of its value ytd, its latest leg down coming on the heels of Fiserv’s disastrous 3q earnings report.”

Exited Positions

First trimmed and then sold out of ( AER 0.00%↑ ), ( GOOG 0.00%↑ ) and SCR.TO: They had strong runs and no longer offered the same return potential as when initially purchased.

Sold all of Barry Callebaut at 1043 CHF. It was a play on cocao mean reverting, and prices have come down… but now I’m worrying about whether that will be enough: will cocao volumes go back to what it was before, or has this crazy spike permanently altered consumer and customer behavior?

Top Contributors

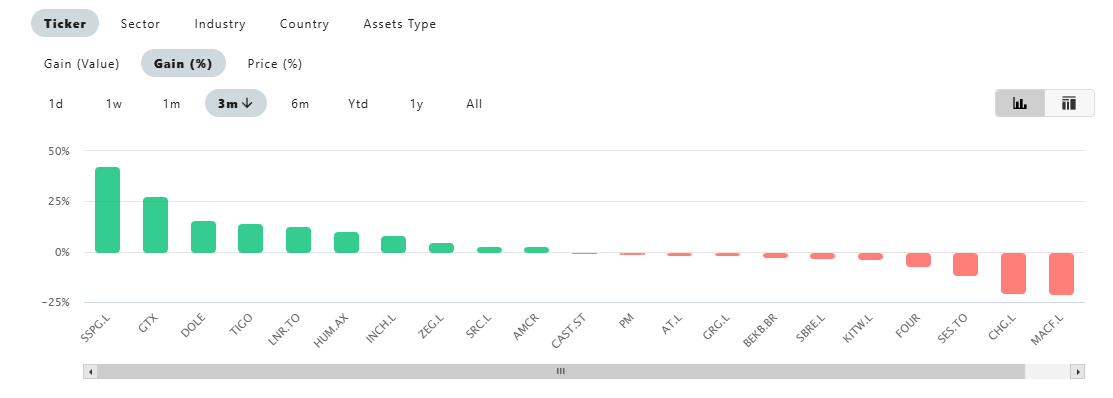

SSPG.L (SSP Group) : +44%

In early December, SSP reported FY25 results showing higher revenue and underlying profit, while noting trading momentum into the new year and guiding FY26 EPS toward the upper end of its range alongside a review/restructuring push in parts of the European rail business. The Q4 move is consistent with a “turnaround is working” re-rating: improving prints, better near-term trading, and renewed confidence in cash returns.

GTX (Garrett Motion) : +27.8%

Q3 was a clear beat with strong margins/cash generation and a raised full-year outlook, and in early December the board authorized a new $250m share repurchase program for 2026. Value stock has turned into momentum.

DOLE (Dole plc): +15%

Cheap stock, good Q3, slight guidance increase and initiation of buybacks.

TIGO (Millicom) +14%

Top Detractors

MACF.L (Macfarlane Group) : -21%

In October, Macfarlane warned that FY25 adjusted operating profit would fall materially short of expectations, following a fatal incident at the newly acquired Pitreavie business and its temporary shutdown. Softer demand and cost pressures also weighed on guidance.

CHG.L (Chemring) : -20%

Good earnings report, so the drop seems more macro/positioning-driven than company-specific. European defence equities saw repeated sharp sell-offs on Ukraine peace-process headlines.

III. Humm Group: Vote at the EGM

IV. Closing Thoughts

I’m of course very happy with this year’s results. And I even managed to do it while reducing my portfolio turnover from 108% in 2024 to 61.5% in 2025. Still high, but progress for me. I’m often tempted by the new latest shiny pitch and am actively working on reducing the amount of transaction I do every year.

That said, this will be the final update of the model portfolio. I started it to build a public track record and generate content for Substack. But it’s become less fun (kudos to people like Memyselfandi007 who have been doing it for sooo many years!) and increasingly a distraction from managing my own PA.

The idea was to go beyond stock pitches and document actual buys and sells in real time. There’s lots of pitching out there, but not much on portfolio construction.

I’ll still write occasionally, depending on mood and ideas.

I have almost hit 1000 subs and a few people even pay, despite all content being free. When I started, I wondered if this could turn into a small side income (and maybe it still could). But I know consistency is key, and I don’t want to force content when I’m not feeling it.

I will keep this space for writing down my ideas when I feel inspired, and connecting with like- minded investors. Not as a potential side hustle.

Thanks Jefke. I think you're making the right call, you'll naturally go through periods where you're more inspired to write.

Chemring potentially falling on peace talks is interesting. Besides the headlines, the two countries seem as far apart as they could be on their negotiating goals.

Also, what's your thinking on trimming Tigo? My rough idea is to trim the first third at around 15x FCF which is also near the 6.2x they paid for all of Guatemala back in the day.

Idea fee tally is…

Congrats on the good performance!