The Trade War Nobody Wins. Except ...

Why tariffs, supply chain cracks, and dollar weakness set up aircraft lessors for another big win

Whenever a shock hits the aircraft supply chain, tightening supply, one group consistently wins: the aircraft lessors.

The logical consequence of Trump’s tariff bonanza is again more pressure to an already strained system, potentially setting the stage for another tailwind for the lessors.

Jeremy Raper on fintwit/finX was one of the first I saw articulate this thesis:

“Anyone w/ metal in the air should be a big beneficiary of even lowish (10%?) reciprocal tariffs.

Aircraft production supply chains are long and multi-national; and basically every OEM is already sold out and w/ shortages for many yrs. Imo logical corollary of cost inflation in the supply chain - inevitable even in a mild tariff outcome - is increased value of extant aircraft, or next-to-deliver (but price-fixed) aircraft.”

And I agree.

On top of that, the dollar has weakened in dramatic fashion vs other currencies, which happens to be another boon for the lessors.

As Pembridge Cap eloquenty wrote:

Owning a bit of gold is nice, but equity in hard assets sitting atop a large stack of fixed rate USD anti-money could be nicer.

AerCap AER 0.00%↑ is my horse in this race, but peers like Air Lease AL 0.00%↑ and Avation (AVAP.L) should also do just fine.

Last week, AerCap’s CEO, Aengus Kelly, appeared on a niche aviation podcast. I always enjoy his insights on the state of the industry, but this time I was especially curious to hear his take on the unfolding tariff situation.

The podcast

I'll briefly highlight the parts of the podcast that stood out to me. These are a mix of direct quotes and light paraphrasing.

Q: How do you view the current trade war and tariff issues?

Kelly:

We buy, sell, or lease more than two assets every 24 hours somewhere in the world and we’re seeing worldwide uncertainty.

Last week, for example, there were concerns about can we bring Leap-1A engines, which power the A320neo, into the US, or will there be a $2 million tariff?

Everyone is saying “hold on, I’ve got a grounded airplane, I need to engine, the parts, or I need to go to an MRO facilility… but I can’t pay the $2M. So we’ll just have to wait and see if things change.”

That’s happening throughout the whole supply chain at the moment, people doing the absolute minimum that they can.

And we all know that this supply chain was already pretty fragile at the best of times. Particularly challenged post-COVID, Boeing’s challenges, quality issues that all the OEMs are facing…

And now, these small companies in the supply chain are really struggling very quickly because the orders they counted on to come in, are not coming in.

We’re not in paralysis, but definitely in first gear. It’s slowing down.

When things slow down in the supply chain as it is, it’s going to create a lot of unintended consequences. The aviation supply chain is not like a pizza oven: you can’t turn it off and back on the next day. It takes a long time to fire it back up again.

Kelly didn’t outright say AerCap stands to benefit, but the message was clear: the longer the disruption, the more valuable existing aircraft and contracts become.

Q: What happens if tariffs force U.S. carriers to pay more for Airbus, and non-U.S. carriers to pay more for Boeing?

(context: US puts 10% tariffs on Airbus & the rest of the world would impose retaliatory tariffs on Boeing)

Kelly:

If the worst-case plays out where the U.S. insists on tariffs on Airbus equipment, than U.S. carriers will have to exit the Airbus fleet over time. They won’t have a choice.

A $5B order going up by half a billion? (10% tariff) That’s the business case gone.

The U.S. will become a Boeing market over time, and the rest of the world will go Airbus. China and Europe won’t sit back (so they will have retaliatory tariffs on Boeing). Boeing ends up with only the U.S., Airbus gets the rest of the world.

Without Europe and China, Boeing isn't viable business. They’ll either have to become nationalized or offshore production: build facilities in Europe and China to compete (e.g. build in EU to escape EU tariffs).

And that’s probably what they'll have to do, because the alternative is a decline into irrelevance.

(That’s also completey counter to what the policy intended to accomplish. Trump wants to reshore manufacturing into the US, but big international companies will have to offshore production meant for export out of the US to nullify retaliatory tariffs )Aviation is one of the industries where the US has a massive trade surplus with both the EU and China (and the whole world).

But in the long run: GE, Honeywell… they will have not choice but the offshore or else they give up the rest of the world to Airbus & Rolls Royce.

Comments on Engine OEMs

Kelly:

The engine guys (manufacturers / OEMs) only get 25% of their sales price in day 1, with delivery. They get their money back with 3 (MRO) shop visits over the life of the engine. The single most important thing is that last shop visit when the aircraft is around 18 years old. That’s all cash. That’s where they make their money.

They never want overproduction. Overproduction would result in the oldest assets being scrapped. Boeing and Airbus just wanna sell as much as possible. They couldn’t care les. The sooner it gets scrapped, the better for them.

The engine guy is the total opposite. He needs the existing technology assets to last. That’s why on a global basis, we never had a prolonged period of oversupply. We have had it in certain markets for a period of time. But on a global basis, it never lasts.

This was already discussed during AerCap’s capital markets day, but I felt it was worth reiterating here.

“The engine guys are a break on supply”

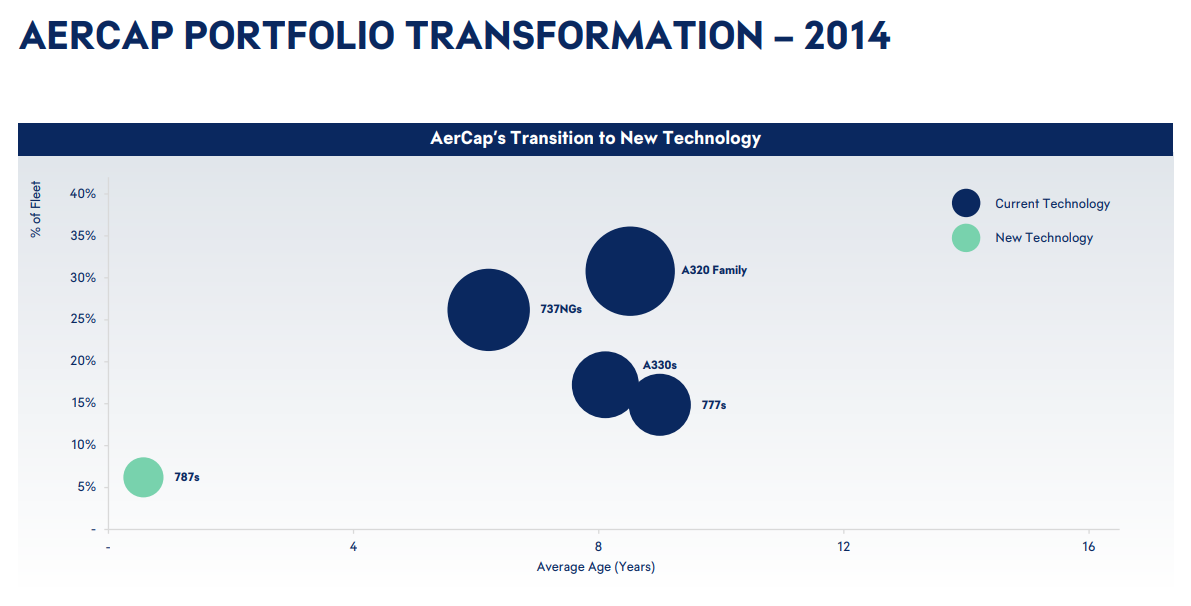

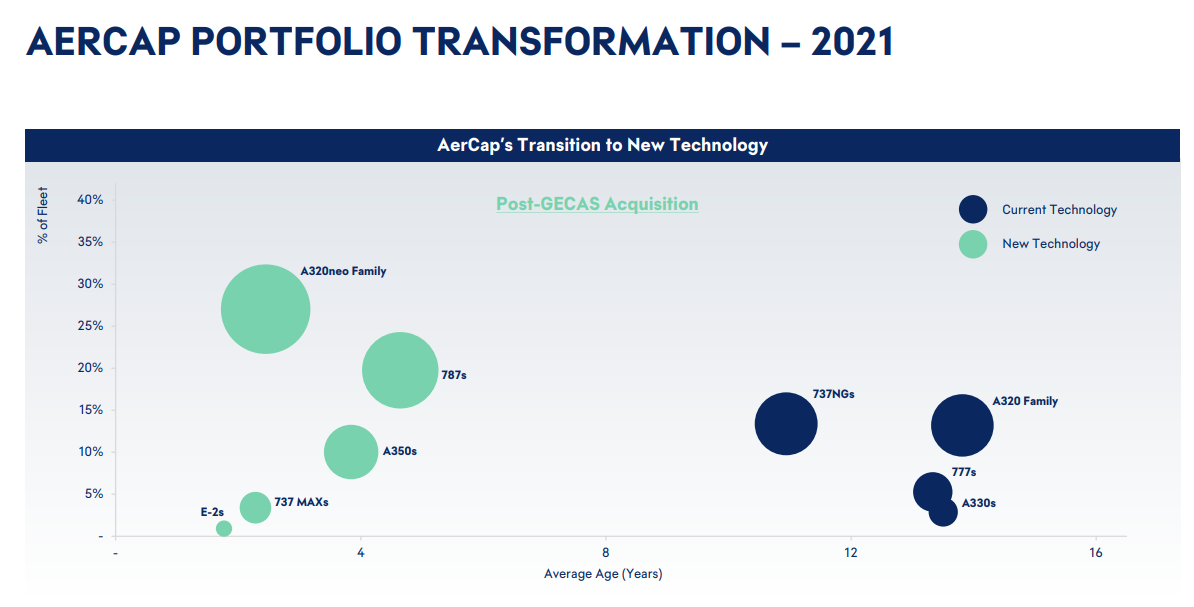

Comments on Ordering Planes - Fleet Age

I found these comments particularly interesting because they touch on a point Air Lease bulls often bring up: that AL’s average fleet age is lower than AerCap’s.

Kelly:

We place speculative orders (= without customer lined up) with Boeing and Airbus, say 100 Maxes or Neos. We’ll have a view of type of aircraft that will be in demand. A view on traffic growth, replacement cycles.

You have to understand how over time demand for an asset changes.

We made a big shift around 2012/13 and stopped ordering older-gen aircraft. There would be strong demand for these until 2028-29. But you need 25 years of demand to make a success in the business case.

If you order a 777 and it delivers in 2015, that needs to be in demand until 2040. We just didn’t see that happening.

We also started exiting those types of aircraft out of our fleet.

You order the wrong asset in this business and you’re stuck with it. It reverberates through the company for the next 15-25 years.

During the Q2 24 conference call, Aengus K. went deeper into the composition of the fleet:

The average age of our sold planes 15 years. The average age of portfolio doesn't matter.

The key is to look at the average age of the components of business. If you have a young fleet of 777s or 737s, you will lose money because those planes will not be flying in 2035, 2038. And if you bought them in 2015, that's what you need to happen.

The average age of portfolio doesn't matter.

AerCap has been actively working on their fleet composition for years. The end result is a fleet that has young new-gen panes and old old-gen. Nothing in between. This is were they want to be and this is where the less constrained business model of AerCap can shine.

Air Lease on the other hand follows a simpler plan:

Buy New Assets Direct from OEMs

Hold Assets for First Third of Useful Life

Sell Assets Re-Invest Capital

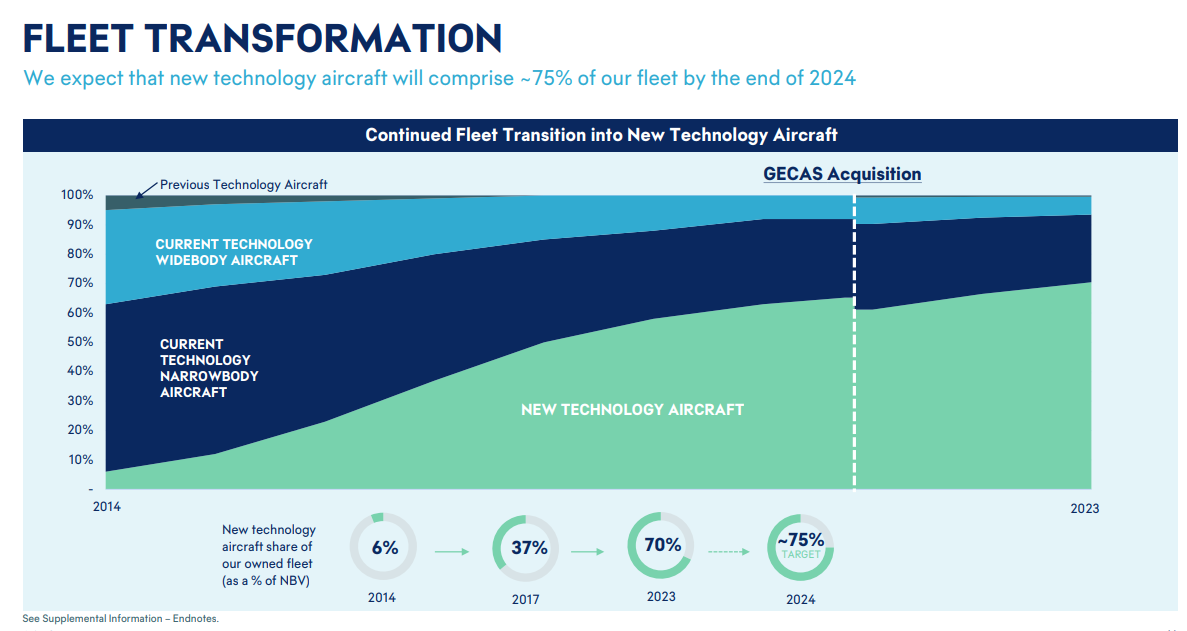

AerCap talked about the evolution of their fleet during the Capital Markets Day in May 2024.

At the end of 2024, 74% of their fleet was new-gen.

Conclusion on AER vs AL

This is just one of many characteristics on which you can compare AerCap with Air Lease. But stocks have avid bulls and I don’t think one side will ever convince the other side to join theirs.

I’m very happy to ride this wave through AerCap. But I wouldn’t be surprised if Air Lease does some catching up once they do some of their own buybacks or actually get acquired.

The aircraft lessors were already enjoying a multi-year tailwind before Trump did his thing. Now tariffs can lead to more supply chain issues and the weaker USD can benefit the holders of hard assets, backed by debt in USD. AerCap reports Q1 2025 tomorrow morning, and I wanted to get these thoughts out ahead of it.

AerCap's fleet composition at the end of Q1 25 from today's earnings release:

As of March 31, 2025, AerCap's portfolio consisted of 3,508 aircraft, engines and helicopters that were owned, on order or managed. The average age of the company's owned aircraft fleet as of March 31, 2025 was 7.5 years (4.9 years for new technology aircraft, 15.2 years for current technology aircraft) and the average remaining contracted lease term was 7.3 years.