V-ZUG Holdings: Temporarily Depressed EBIT Margin = Opportunity?

If management can return to a 10%+ EBIT margin, this stock could be on its way to compounderville.

THESIS

V-ZUG’s earnings got crushed due to a barrage of temporary & mean reverting issues (shortages, delivery delays, increased material & freight costs…). Recovering from that will show that the stock is cheap.

If management manages to hit their medium term target, we get a bunch of growth on top.

Then this becomes an attractive story of

10%+ ROE,

increasing ROE,

EBIT % expansion,

“hidden” growth engine inside bigger low-to-no growth business,

20-40% of earnings paid out as dividend

A recipe for multiple expansion.

The stock trades at an EV/NTM Revenue of 0.62x. Usually I wouldn’t use metrics like this, but it’s useful when working with temporarily depressed profit margins.

Quick Valuation

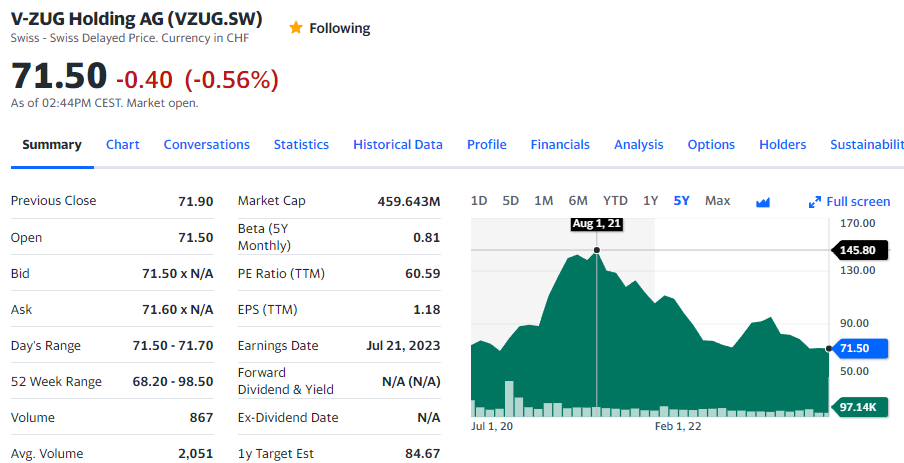

At CHF 71.50 per share, the company has a market cap of CHF 460m and an EV of about 400m. LTM revenue of 640m. Current, depressed EBIT is 10m.

This a company that hit 60m+ EBIT many times in the past, with an average EBIT margin of 10%.

Slap an 10% EBIT margin on current revenue, and we have EV/EBIT = 6.25. V-ZUG likely won’t hit that 10% this year, but it seems very reasonable to believe that they will do so again soon.

I think the stock is cheap and bought a position at CHF 71.50

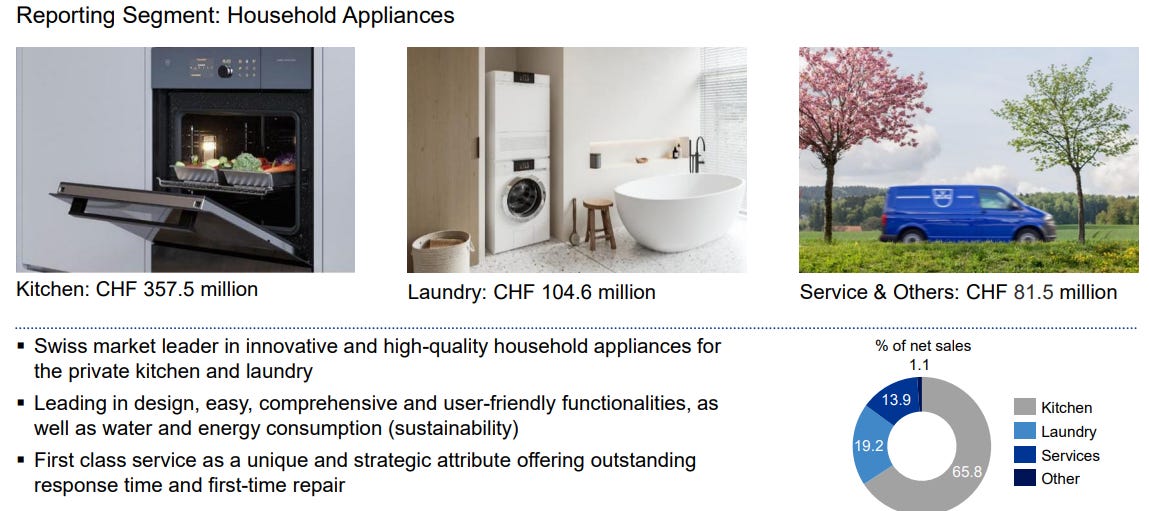

What’s a V-ZUG?

Swiss manufacturer of mostly fancy, high end kitchen appliances.

In 2019:

Their sales are mostly domestic, but with a growing international portion.

Swiss market (82% of revenue in 2022) premium & medium/advanced segment

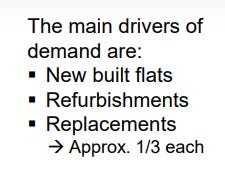

Partly driven by energy saving measures, construction activity in the new-build industry - including refurbishments of existing building stock - is expected to remain at a high level, so the outlook for renovations continues to be positive.

The replacement business remains virtually unaffected by the economic cycle and is benefiting from an already large installed base.

(FY23 Outlook given in March 2023)

International: premium product range only

Market share is still small, considerable potential for above-average sales growth.

THE SPIN-OFF

V-ZUG was spun off from Metall Zug in June 2020. This was combined with new shares issuance = capital increase for CHF 110m. Share price opened at CHF 72.

Household appliances (= mostly V-ZUG) was 90% of revenue for Metall Zug in 2004. But other segments kept growing, and after a bigger acquisition in 2018, it was time to spin-off V-ZUG.

The planned spin-off and listing of V-ZUG will significantly change the profile of Metall Zug. The changed Metall Zug will be a more strongly focused industrial group and essentially be active in the two growing markets of medical technology and wire processing.

Metall Zug kept 30% of shares, various insiders have big stake.

The Pitch in 2020, after the Spin-off:

V-ZUG has stable sales in Switzerland but is working on international expansion and investing in new factories.

The reason given for the spin-off was:

As an independent listed company, the V-ZUG Group can further strength the brand and visibility & benefit from additional strategic flexibility.

To me it seems the spin-off was done because of the expansion plans: raise some capital and prevent the potentially temporarily depressed earnings/cash flow to mess up the results of Metall Zug.

Goals

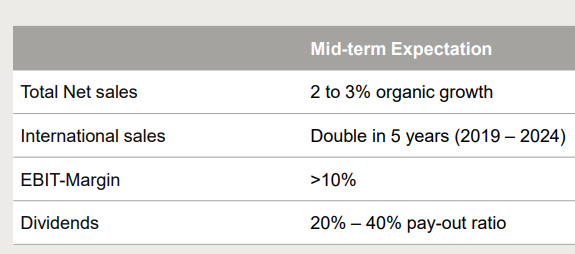

International sales is 10% of revenue. The goal is to double it in 5 years.

Lower profit in 2019 due to higher OPEX related to new ERP integration, but goal is to go revert back to “normal” 10%+ EBIT margin. This should be attainable, since it seems like the household appliances segment within Metall Zug has averaged > 10% EBIT margin since 2004.

A dividend will be considered 3 years after the spin-off.

New Factories

New refrigeration production plant in Sulgen

New vertical factory in Zug: “Reduction of throughput time up to 50%”

Simultaneously implementing these projects calls for exceptional efforts and generates overlapping costs. However, they should ultimately allow the Business Unit to maintain its position of technological leadership and operate more efficiently

After completing these investments, V-ZUG will have state of the art production capability and capacity to grow SUBSTANTIALLY and profitably

A Timeline of Margins Getting Crushed

The stock has been a wild ride. After the market believed that the lower earnings in 2019 were only temporary, the share price doubled. But this would not last.

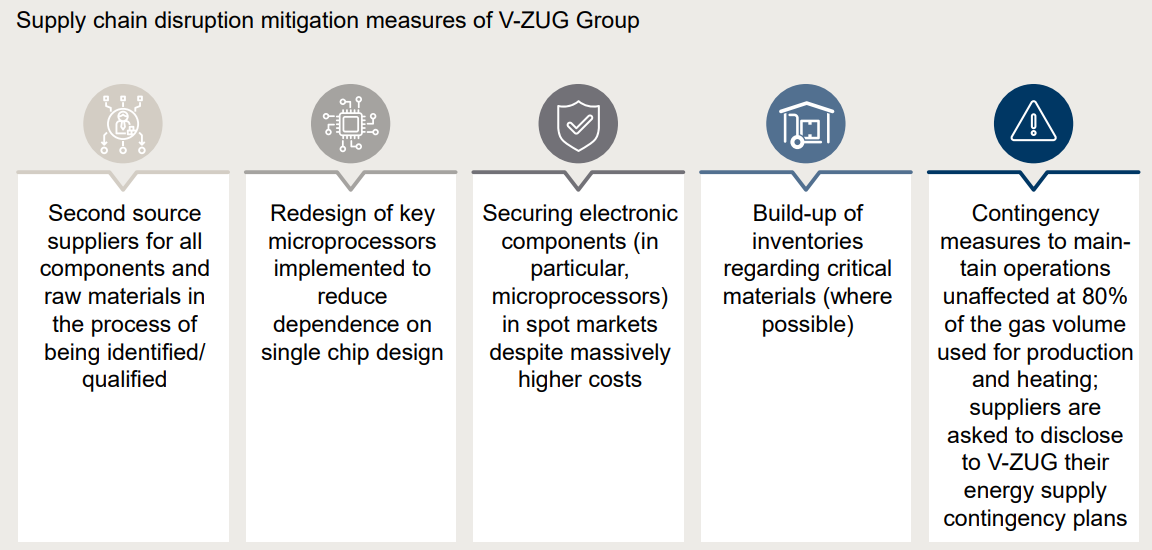

While V-ZUG was initially not impacted by all kinds of supply chain issues in 2020 & 2021, 2022 proved to be different.

March 2022 (CHF 110)

After record results in 2021 (with 10% EBIT margin), they mentioned that they were currently dealing with supply chain issues (material & freight cost inflation ). But V-ZUG was still “aiming” for a 10% EBIT margin in FY2022.

May 2022 (CHF 90)

Profit warning, but they mention a strong order book.

Despite sustained high demand, supply chain bottlenecks and further rising procurement costs will affect the V-ZUG Group’s net sales and operating result in the first half of 2022

HY22 Results in July 2022 (CHF 78)

Sales ok, but EBIT margin crushed to 1.4%

Cost increases, component shortages and delivery delays all impacted the operating result

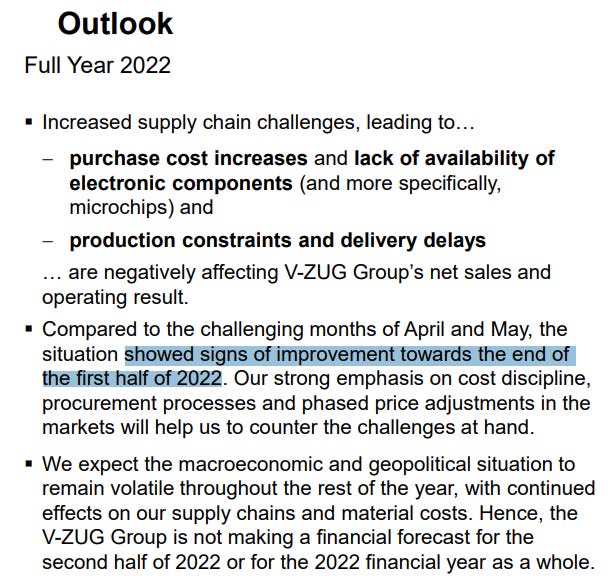

V-ZUG Group is not making a financial forecast for the second half of 2022 or for the 2022 financial year as a whole.

The outlook for a continued strong demand in all its markets therefore remains generally optimistic. The significant increases in procurement costs will be passed on to customers in the form of gradual price increases. However, these increases will be delayed by around three to four months

Updated (improved) Goals

FY22 Results on 15th of March 2023 (CHF 80)

Sales were stable, but the EBIT % was only 1.6

The EBIT margin fell to 1.6 % (previous year: 9.9 %) with net sales at a similar level to the previous year. This development is primarily due to lower sales volumes as a result of delivery delays, soaring procurement prices for almost all purchased materials and freights, as well as inefficiencies in production caused by the supply chain problems.

They mention gradual easing of the issues in second half of 2022. And reiterate medium-term targets of 3% organic sales growth, 10-13% EBIT margin.

The earnings are currently depressed by a variety of issues that should have bottomed and be mean reverting:

Supply shortages & delivery delays

Increased Freight & Material costs

Or said otherwise: number go up again.

Cyclical?

It seems like V-ZUG sales should be impacted construction activity. And rising interest rates are no bueno.

However, they still saw strong demand when they produced their FY23 outlook.

Domestic: Partly driven by energy saving measures, construction activity in the new-build industry - including refurbishments of existing building stock - is expected to remain at a high level, so the outlook for renovations continues to be positive.

The replacement business remains virtually unaffected by the economic cycle and is benefiting from an already large installed base.

International: Market share is still small, considerable potential for above-average sales growth.

And V-ZUG sales inside Metall Zug actually grew during 2008 & 2009.

So I can’t really pinpoint why, but sales have been holding up pretty well in the past.

Bear Case - Things to Watch Out For

Could we see a bigger slowdown in sales than we’ve seen in the past?

How good is management’s ability to forecast? The following sequence didn’t really inspire confidence:

March 2022: still aimed for 10% EBIT for FY2022. End of May: profit warning

July 2022: 1.4% EBIT margin, but saw “signs of improvement”. FY22 EBIT %: 1.6%

However, the excuses seem reasonable. These factors should have bottomed now and mean revert automatically.

How fast can they revert back to 10% EBIT Margin? Did the last year change something structurally with permanently lower margins as a consequence?

New factories & international expansion can come with growing pains.

Why Does the Opportunity Exist?

Small cap with low liquidity (trades $160k / day on avg)

Current earnings are crushed

Current FCF disappears into capex & inventory

What Does a Successful Outcome Look Like?

When (If) the EBIT margin goes back up, we’ll see a nice company with growing earnings, margin expansion and good ROE.

In 2024 - 2025, the biggest new investments will be behind them. V-ZUG will have room to optimize and grow into the new asset base = growth requiring less capital.

This seems to be a recipe for multiple expansion. If V-ZUG’s own historical valuation can be any guide, an EV/EBIT of 11-12 looks quite reasonable.

If we don’t get the bonus of rerating, we’ll still have a cheap stock trading at 8-10 P/E, by then paying out 20-40% of earnings as a dividend.

BONUS: UBER BULL

Let’s speculate about what a better than expected outcome looks like:

VZUG raises prices with a lag. Input costs go down, they maintain increased prices: improved margins beyond what they had in the past.

Accelerating growth after 2026 than the 3% in the medium turn plan (2023-2026), after both new factories are up and running.

Conclusion

This is not necessarily my “fattest” pitch, but I felt like it was an interesting stock to write up since I don’t see it mentioned anywhere.

It initially popped up on my radar some years ago thanks to Michael Fritzell from Asian Century Stocks.

I bought it early 2021 and sold it a couple of months later, after decent earnings and a quick 25%+ gain. I think it’s time for round 2.

(Half-Year Results 2023 will be published on July 21, 2023)

As this is my first public write-up, I appreciate all of your feedback! This can be about the company & stock, but also about the way this post is structured or written.

I want to give myself the option to do quick stock pitches in the future, so I don’t wanted to do the deepest of dives. That said, this post ended up being longer than originally planned. I hope you got something out of it!

Disclaimer: The information provided in this blog post is for informational purposes only and should not be construed as financial advice. The opinions and analysis expressed are solely based on the author's personal views and research. Investing in stocks involves risks, and the value of investments can fluctuate. Readers are encouraged to conduct their own research and consult with a qualified financial professional before making any investment decisions. The content presented here should not be considered as a recommendation to buy, sell, or hold any securities. The author does not guarantee the accuracy, completeness, or reliability of the information provided. Past performance is not indicative of future results. Each individual's financial situation and risk tolerance may vary, and readers are responsible for their own investment decisions. The author assumes no liability for any losses or damages incurred as a result of the use of this information.