V-ZUG Half-Year Report 2023

Long term goals reiterated, but short term issues delay progress.

Summary

“Improved results with stable sales development” is how V-ZUG titled their press release for the results of the first Half Year of 2023. Too bad that improved here means going from 1.4% EBIT margin to 1.7%. Not the improvement I was counting on.

Although management didn’t see any demand problems 4 months ago, they are now “suddenly” hit with them.

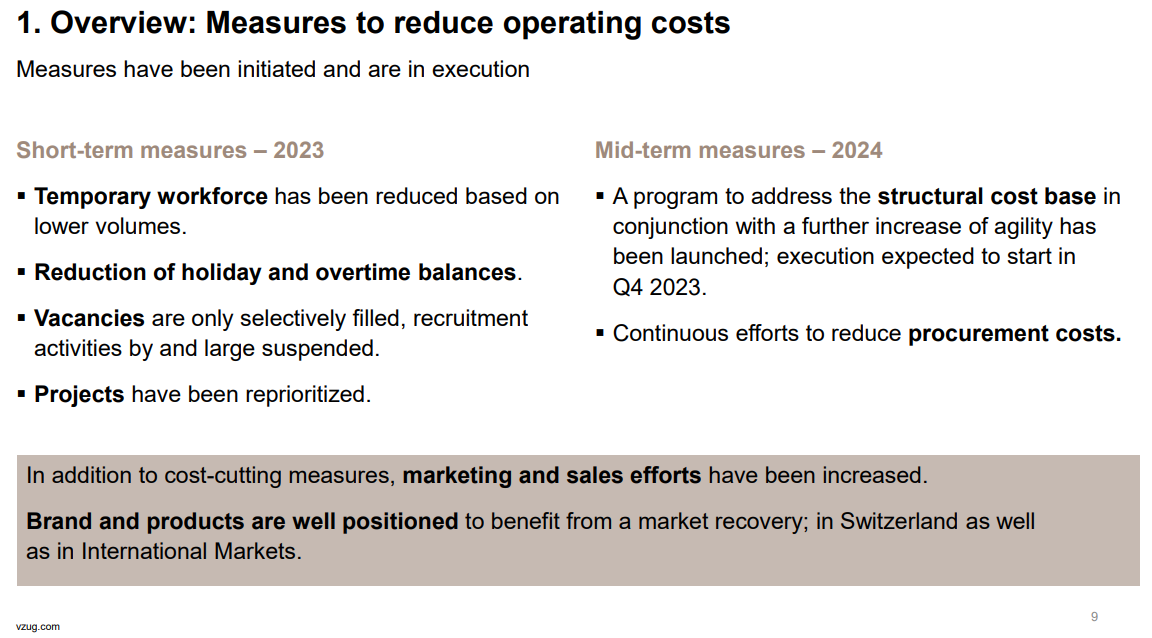

Will cut costs

No FY 2023 outlook

Resources:

The Good

Overall sales down only 1.6% compared to H1 2022. Good growth in international markets (+13%). International is now 20% of total sales.

Back to unrestricted delivery capacity since February 2023.

The Bad

Lower Demand

In the first half of 2022, component shortages and delivery delays impacted net sales.

… purchases on spot-buy markets, could be avoided to a large extent. V-ZUG is back to unrestricted delivery capacity since February 2023.

Finally back to “unrestricted delivery capacity”, but now hit with lower demand.

In the first half of 2023, demand for household appliances fell year on year due to uncertainty about the geopolitical situation as well as factors affecting investments such as rising interest rates and inflation. Moreover, the inventories of customers were still well stocked, which put further pressure on volumes.

This has an impact on EBIT.

However, EBIT improved on a low level, as operating expenses had to be allocated to lower volumes

But remember that in their FY23 outlook given just 4 months ago, V-ZUG saw no issues in demand. Back then they announced:

Domestic: Partly driven by energy saving measures, construction activity in the new-build industry - including refurbishments of existing building stock - is expected to remain at a high level, so the outlook for renovations continues to be positive.

This makes me question management’s forecasting abilities (maybe shifts in demand are so abrupt that they can’t give accurate forecasts) or management paints a rosier picture instead of being transparent with investors.

Cutting Costs

The V-ZUG Group is addressing this development with sales-increasing and cost-saving measures. Continuous efforts are being made to lower procurement costs, the number of temporary jobs has been reduced, vacancies were only selectively filled and recruitment activities by and large suspended. Projects have been reprioritised and expenditures cut.

While I applaud being nimble to ease the pain of lower demand, cutting costs seems contradictory to V-ZUG’s plan of building a new factory to increase capacity.

In addition to the cost-saving measures already mentioned, various measures were also introduced to improve sales.

I don’t know what this exactly means, but I have a feeling it will not be beneficial to earnings, at least short term. Increased marketing spend or lowering prices are the first things that come to my mind.

Lack of FY 2023 Outlook

There is plenty of talk about sustainability in the letter to shareholders, but not a word about the full year outlook. Even in the horrible 2022, they announced that they had no forecast.

From the HY1 2022 PR:

Outlook

… We expect the macroeconomic and geopolitical situation to remain volatile throughout the rest of the year, with continued effects on our supply chains and material costs. Hence, the V-ZUG Group is not making a financial forecast for the second half of 2022 or for the 2022 financial year as a whole.

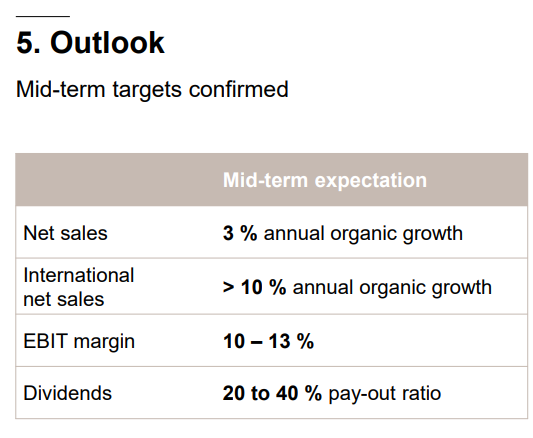

V-ZUG did reiterate their “mid-term” targets in the investor presentation.

But what is mid-term? In July 2022, these targets were explicitly for 2023-2026.

Conclusion

I found the recent earnings disappointing. Fundamentally, I was hoping for an improvement in EBIT margin this half-year, a step in the direction of their long term goals.

Additionally, I have concerns about the management's communication with shareholders. It seems either they are not forthcoming about negative aspects or have difficulty making accurate forecasts.

Although I believe V-ZUG will eventually achieve its stated goals, a decrease in demand will delay the process. The lack of outlook for FY 2023 leads me to believe that the second half of the year could be really bad.

Maybe we get an amazing recovery in 2024, maybe we won’t… I’m just a retail investor doing no deep dives on substack. I decided to not stick around and find out and sold my position today below the current trading price of CHF 71.

Buying, Selling & Holding Period

I feel weird writing up a stock only to sell it a couple of weeks later. Ideally my holding period would be longer than … three weeks.

But on the other hand, a common pitfall of publicly talking about a stock is that you feel married to the position. I want to make sure that I'm not. As a private retail investor, I have the flexibility to enter and exit positions quickly.

Maybe I need to rethink the kind of stocks I will write about in the future, to prevent situations like this.

Disclaimer: The content provided in this blog is for informational purposes only and should not be considered as financial advice. Investing in stocks carries risks, and readers should conduct their own research and seek professional advice before making any investment decisions. The author may hold positions in the stock being discussed or other related investments. Any views or opinions expressed in this blog post are subject to change without notice and should not be construed as a recommendation to buy, sell, or hold any particular security or financial instrument. The author and the blog, including its affiliates, partners, and employees, shall not be held liable for any errors, omissions, or losses incurred as a result of using or relying on the information provided in this blog.