Your Stock just Dropped 28.6%. Now What?

Navigating the Aftermath of Bel Fuse's Earnings Tumble

On February 22nd, Bel Fuse (BELFB 0.00%↑) dropped a whopping 28.6% , plummeting from $70.11 to $50.02 following their Q4 '23 earnings release. If you’re anything like me a drastic drop like this will always seem like an overreaction and you’ll be fighting the urge to buy the dip.

Let's take a closer look.

Investment Pitch Pre-Earnings Report

I wrote up Bel Fuse in a previous Substack post.

The stock pitch was relatively simple:

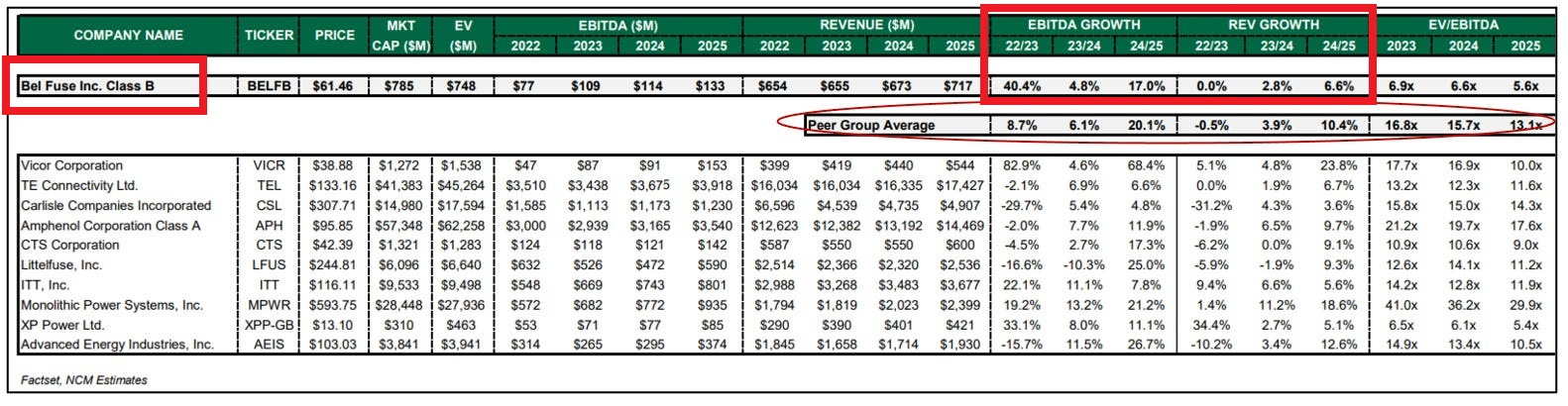

Bel Fuse was trading at a discount compared to its peers, primarily due to its lower profit margins. The appointment of a new CFO, Farouq Tuweiq, marked a turning point towards prioritizing profitability. Consequently, Bel Fuse saw significant EBITDA growth outpacing the sector in 2022 and 2023. As profit margins narrowed the gap with its competitors, the argument for a lower valuation multiple weakened. Every quarter confirming the improved margins increased investor’s confidence in their structural nature.

This combination of EBITDA growth and multiple expansion would lead to an explosion in stock price. Although most of the margin expansion juice has been squeezed out of the stock by now, as highlighted in my write-up, the increase in stock price was driven solely by earnings growth, not yet by multiple expansion!

But to sustain the recent momentum, a return to revenue growth is necessary at some point.

And that's why the latest earnings report had such a dramatic impact.

The Earnings Report

Sales and EBITDA in Q4 ‘23 were a bit lower than expected, but the gross profit margin was a stunning 36.6%, again confirming the structural change in profitability.

FY 23 results were pretty good:

Revenue: 640m

Gross profit margin: 33.7% (vs 28% in 2022)

Net earnings: $73.8m (vs $52.7m)

Adjusted EBITDA: $110.5m (17.3% margin) (vs 83m (12.7%) in 2022)

To put these numbers into context: there are about 12.8m shares (A+B shares) outstanding. Using a B share price of $50.25 to calculate the market cap results in 643.2m. With about $67 net cash, the EV is $576m.

This translates to an EV/EBITDA = 5.2x and P/E of 8.7x based on TTM results.

But the problem with report wasn’t the FY23 results, it was the forecast of a slow start in 2024. The company projected Q1 ‘24 sales between $125m and $135m, below the TIKR estimates of $145m. A potential rebound would only be on the second half of 2024, so that also implies a guide down for Q2 ‘24 compared to estimates.

How Big of an Issue is this?

The slow start in 2024 kind of destroys the momentum dream of continued YoY EBITDA growth. The market hasn’t seen sales growth during the turnaround in the company, and the H1 ‘24 revenue guide down casts doubt on those prospects.

Before the earnings report, analysts estimated 4.8% EBITDA growth in 2024 and 17% in 2025, as referenced in this overview:

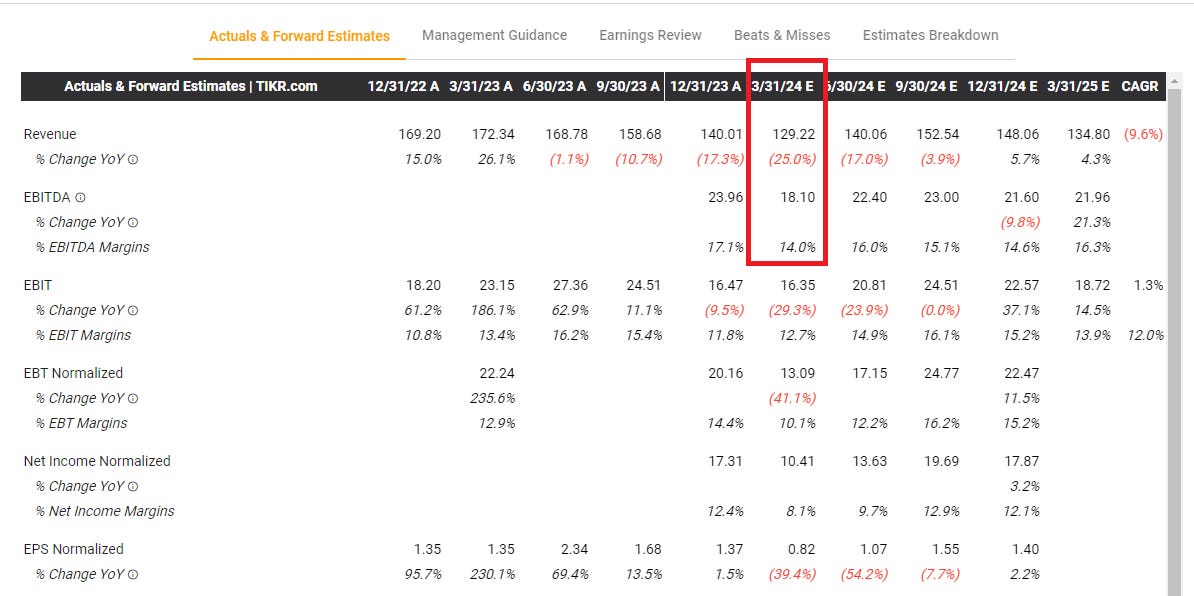

But after the last earnings call the pendulum swung to:

Could EBITDA actually be down YoY?

We have seen the company improve margins. But can they grow sales again?

From a “flows” perspective (as in: money flowing in and out of stocks, as opposed to fundamental investing) this is a problem for the stock. It kills the momentum of YoY growth. It could lead to analyst downgrades. It makes it a harder story to sell to new investors.

I think the stock price deserved to go down here and that’s why I didn’t immediatey buy the dip on day 1.

But the real question, at least if you’re trying to be a longer term fundamental investor, is: how much does this slowdown impact the intrinsic value of the company?

This very timely post written by

helps us think through that question:

The author writes how massive moves after earnings at first sight seem like evidence of short-termism. But, he argues, investors actually make a different error:

However, the error these investors are typically making doesn’t have to do with having a short-term mindset, but rather overextrapolation.

As we all know, a stock is simply partial ownership in a business and a business is simply worth the sum of all future cash flows discounted back to today. In theory, if no other assumptions in an investors “DCF” changed, then a 3 cent miss would only reduce the value of each share by 3 cents.

When we see a stock down 8% on a slight earnings miss, what investors are actually doing (if we are generous) is extrapolating out this incremental data point from earnings and compounding its implications across the entire future of the company. Of course, when you compound anything long enough, even small changes can have large impacts.

This is why a small change in earnings expectations can result in a large change in the company’s market value. The change in value is driven by long-term predictions, but the assumptions are susceptible to noise.

Applied to Bel Fuse: when the guidance for a slow start in 2024 gets extrapolated throughout the whole (literal or implied) DCF, the effect on stock value can be massive. But how much does it alter the earnings power of the business in 3-5 years?

While the stock price may move wildly in the short-term for a myriad of reasons, the long-term value of a business is far steadier. When a long-term investor invests in a stock, they are looking to the long-term prospects of the underlying business, not the beliefs of other market participants as to what they expect the stock to trade at. They are looking to make money by buying a stake in a business and holding it as it becomes more valuable, not by selling the stake to another market participant at a higher price.

Now I’m not saying to ignore any new info. Part of the Bel Fuse thesis is a return to revenue growth. This is a key point I wil keep my eye on and we just saw a data point that doesn’t support the bull thesis. So a drop in share price is justified.

Now it’s not that the incremental data point never has any long-term ramification, but rather that the data set is typically too small to reliably draw anything intelligent. Said simply, there is too much noise in a single quarter’s results.

However, string together a few quarters of similarly poor results and you may be able to see a pattern, which an investor considers significant enough to draw a conclusion from (i.e. signal).

However, a drop of 28.6% appears to be an big overreaction to what was actually reported. After reading the earnings call and talking about it with some other investors, I gathered my thoughts and concluded that I will buy the dip after all. And that’s what I did.

(FYI: I post the trades in the model portfolio live on Substack Notes.)

Updated Analyst Estimates

As I wrapped up this post, I noticed updated analyst estimates on TIKR, reflecting the latest guidance from Bel Fuse. Everything I wrote above is without taking that new info into account. Earlier estimates showed about 3% in revenue growth and a 2024 EBITDA of $113m.

It seems like analysts used the new guidance to make big cuts:

The new estimates are even more negative than the actual guidance Bel Fuse provided. After all, they said Q1 ‘24 would have the same margins as FY2023. This would imply an EBITDA of $22m instead of $18.10.

But we’re losing track of what matters. We have to remember that our core focus isn't fine-tuning short-term earnings predictions.

And even if the new estimates for FY24 would be 100% accurate, how much does that change the intrinsic value of Bel Fuse, which is the discounted sum of all future cash flows?

The answer is not straightforward. Is this hiccup a temporary blip, or does it signal a negative revision to the long term earnings power of the business?

The truth is probably somewhere in between.

The slowdown is a data point that works against the company for the “return to sales growth” thesis. But it’s just one, and extrapolating it through 2024 and 2025 seems like a stretch.

Analyst estimates now imply a stock price below 10x P/E, ex-cash, on trough(ish) earnings. That’s a cheap stock, especially when they intend to put the cash to work. But the real re-rate will likely only happen when the company returns to sales growth.

Given how mismanaged the company was before and how easy it seemed for Farouq to pull some levers and increase profitability, I can’t imagine it being too hard to find some ways to increase the top line.

Management is aware of this, and it will be their main focus for 2024.

Disclaimer: This content is for educational and entertainment purposes only and is not intended as financial advice. Perform your own research and consult a qualified financial advisor. The author may hold positions in the discussed stocks. This is not a recommendation to buy or sell securities.