The kick off the new year, I thought I’d share a couple of words about each position in the model portfolio.

The portfolio delivered a 27.8% return in 2024. I’ll be publishing a separate "year-end letter" to recap its performance in more detail.

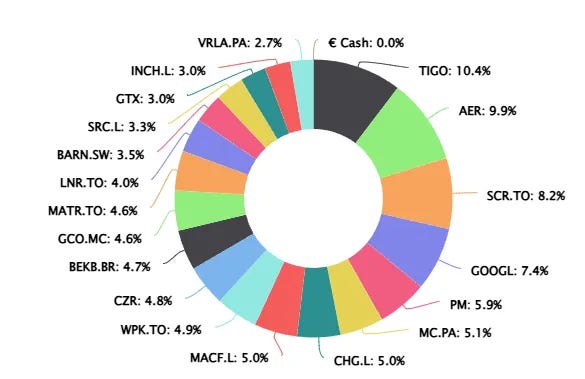

Here’s how the model portfolio looks like on January the 1st:

Disclaimer: This content is for educational and entertainment purposes only and is not intended as financial advice. Perform your own research and consult a qualified financial advisor. The author may hold positions in the discussed stocks. This is not a recommendation to buy or sell securities.

The Portfolio

1. Millicom ( TIGO 0.00%↑ )

I have written and tweeted extensively about Millicom, and it remains my favorite and largest position going into 2025. This Latin American telecom company is attractively value not just on EV/EBITDA, but also on actual free cash flow (FCF). This, in combination with the recent monetization of tower assets, gives it ample cash to work with the coming years. They just started a share buyback program, paid out a special dividend and intend to initiate a regular recurring dividend in 2025.

Despite the stock being up 38% in 2024, it’s still as cheap on NTM numbers as it was a year ago. This is due to FCF estimates being raised throughout the year: $700m FCF in 2025 at the current market cap of $4.2B leads to a 16.5% FCF yield, which is about the same as when I initially wrote up the stock at $19.

has a big recent post on the current state of Millicom, and here’s what I have written about it in 2024:

2. AerCap ( AER 0.00%↑ )

The world’s largest aircraft lessor currently benefits from a global aircraft shortage due to underproduction by Boeing and Airbus, as well as engine reliability issues limiting aircraft availability. This dynamic increased the value of the assets already out there, like AerCap’s fleet.

The company currently trades at 8.2x fwd P/E and a tad over book value. This BV understates the true value of the assets as AerCap regularly sells planes above BV. The company takes advantage of their cheap stock through aggressive share buybacks. Historically 1x P/B has been the ceiling for the stock, but given the current tailwinds and understated asset values, fair value can easily be 1.5x P/B or more.

3. Strathcona Resources (SCR.TO)

I don’t love oil right now, but seems like no one does… and that’s a setup that will always peak my interest. On top of that, I usually like to have some oil in my portfolio: it can zig when other sectors zag. Within oil, I’m often drawn to Canadian oil sands for their low decline, low capex assets that offer a lot of flexibility. My “safe” oil sands play used to be CNQ 0.00%↑ , but recently I stumbled on Strathcona Resources which has taken its place.

Strathcona Resources is a funky Canadian oil sands company offering low-decline, low-capex assets and trading at a discount to peers. It was private equity origins and the free float is only 9%. In November they hosted their first Investor Day, and management outlined plans to grow production at 8% CAGR over six years while generating CAD $26/share in excess FCF (~87% of its current CAD $30 share price) at $70 WTI.

They currently have a base dividend of 3.3% and seem to be hinting at special dividends as the initial way to return excess cash. They think their stock is cheap, but buybacks are not the way to go with the limited free float.

4. Alphabet ( GOOGL 0.00%↑ )

No deep insights here: feels unloved because of antitrust overhang and tech bros seem to see it as an AI loser (“I only use perplexity, bro!”).

The company is expected to compound earnings at 10%+ annually. I can easily see this turn into a perceived AI winner accompagnied with some multiple expansion.

5. Philip Morris ( PM 0.00%↑ )

This tobacco giant has been well positioned for smoke-free nicotine growth for years. But what made me finally pull the trigger was Zyn going crazy. It is a small part of overall business, but rejuvantes the growth that had slowed down: now projecting 9%+ EPS CAGR, while paying a 5% dividend.

6. LVMH (MC.PA)

Global luxury leader and compounding powerhouse, facing headwinds from China and luxury market slowdown fears. I occasionally dip my toes into the stock when there are temporary hiccups. Buying the dip in a temporarily out of favor compounder. While recovery from current fears may take time, the company’s long-term prospects remain intact.

7. Macfarlane (MACF.L)

UK-based packaging company, relatively stable but currently facing a small slowdown in revenue.

Macfarlane remains a cheap, steady business at about 9.2x forward P/E, but a re-rating will depend on resuming growth. M&A remains the focus, although I wish management would also consider share buybacks at the current low valuation.

8. Chemring (CHG.L)

A small cap UK-based global manufacturer of defense technology products. It had a couple of operational hiccups YTD, but a filled order book and is expanding capacity. The current valuation of 16.8x fwd P/E is about its historical average, but the outlook is definitely above average: restocking of supplies because of UKR/RUS, increased defense spending for EU countries…

We might be looking at decade long tailwind that’s not priced in, with strong (15%+) EPS growth in 2026 and beyond.

9. Winpak (WPK.TO)

North American leader in packaging materials and machines, with a cash-rich balance sheet and improving capital allocation.

The company was brought to my attention as a new position for Upslope Capital in Q2 24. Upslope has been following the packaging sector or quite a while, so my interest is always peaked when he has a new pick.

Winpak trades at 12x NTM P/E, with earnings expected to grow the next couple of years, after some recent increased capex. I’m not a fan of a lazy balance sheet with a big net cash position, but this Winpak is a story of improving capital allocation. They started their first share buyback in 2024 (5% of shares) and plan to renew the authorization next year. On top of that, they recently announced $3 special dividend (6% yield).

10. Caesar’s Entertainment (CZR)

Casino and hospitality operator with a volatile stock, now trading at yearly lows despite improving fundamentals.

Lots of gaming stocks are interesting, but CZR 0.00%↑ stands out because of inflecting FCF generation for 2025-2026+ as elevated capex winds down and its digital segment keeps growing and contributing more to earnings.

Management has signaled they will start buying back stock once leverage targets are met, expected around Q4 24. They have already done a small buyback after the monetization of a non-core asset.

The stock is a “show me” story and so far the company results haven’t really convinced the market just yet. The thesis remains intact, but this is one stock where the stock price going down actually influenced how I feel about the investment. I know this shouldn’t be the case… but it is.

11. Bekaert (BEKB.BR)

Bekaert is a global company that specializes in steel wire transformation and coatings. It’s undergoing a transformation under new management, focusing on margins, ROCE, and cash generation. Just like Winpak, this is a story of improving capital allocation.

Bekaert is shifting its portfolio toward higher-margin, growth markets. Despite a small guidance cut, the stock trades at just 6.5x forward P/E on these new estimates.

Management has shown discipline regarding capital allocation: they restarted buybacks after finding no accretive M&A opportunities. I love this flexibility in capital allocation: both M&A and buybacks compete for the company’s cash, and you should just pull whichever lever is most appealing at the time.

did an in depth write-up:

12. Grupo Catalana Occidente (GCO.MC)

One of 2 big players in global credit insurance (good!) , but comes with "ok" regular insurance company attached.

The company trades at ~7x P/E and 0.83x BV. I think of GCO as a relatively safe play, wtih returns coming from a 3.6% dividend yield and moderate earnings growth from reinvesting at hopefully the longer term average ROE of 12%. Management seems committed to a growing dividend, but it would be nice if they’d consider share buybacks the current low prices!

13. Mattr (MATR.TO)

Over the last couple of years, Mattr has undergone a major business transformation: it sold of some of the more cyclical O&G exposure to focus on more critical industrial and infrastructure-oriented businesses. This pivot included heavy investments into organic growth with elevated capex spend in 2023 & 2024, topped off with an accretive acquisition in their new area of focus.

The company has set ambitious organic (pre-M&A) targets: >10% revenue growth, >20% EBITDA margins, and >70% FCF conversion. If they come even close to these goals, the stock could be an absolute homerun

So why is it cheap today? There’s no guarantee these bullish plans will materialize. Visibility remains limited in some areas, and 2025 could still be a challenging year. But they are expanding and buying back shares in current weakness, making them ready to capitalize on a return to growth.

14. Linamar (LNR.TO)

Canadian industrial trading at about 6.5x fwd P/E & 15% FCF yield. It consists out of a mobility (car related) and an industrial segment (mostly agriculture). Both segments are in a downcycle, but estimates are stable for 2025 with a big jump in 2026. Historically a solid operator, but hesitant to buy back shares. The new CEO has listened to shareholders and they recently started a big buyback program. There was also a big (3m CAD) insider purchase in December 2024.

15. Barry Callebaut (BARN.SW)

Leading outsourced chocolate producer, navigating temporary headwinds from skyrocketing cocoa prices. A big player like Barry is likely to pick up market share in the current crisis. Currently available at “trough on trough"(low multiple on low margins). Input costs should mean revert eventually. While FCF is pressured by a working capital buildup, eventual input cost normalization should drive recovery.

In depth write up from last year here:

16. SigmaRoc (SRC.L)

SigmaRoc is an EU aggregates/limestone operator that transformed itself by acquiring the European assets from CRH.

The stock appears very cheap, but there's a catch: SigmaRoc is a serial acquirer that consistently directs investors' attention to adjusted EPS. But this time, after their biggest acquisition to date, they pinky promise us that future acquisitions will be limited to smaller tuck-ins, and “one-time” costs will decrease. If true, we should see adjusted figures converge to unadjusted numbers.

You can read an in depth stock pitch on VIC.

17. Garrett Motion ( GTX 0.00%↑ )

Leading turbocharger supplier with a cash-generative model, undervalued amid terminal value fears and shareholder overhang.

Garrett trades at ~5.5x EV/EBITDA (2024E) and an ~18% FCF yield. After buying back a ton of shares in 2024, they recenty announced a capital allocation policy of returning 75%+ of FCF via dividends (2.7% yield) and share buybacks.

The stock has been fighting an uphill battle of terminal value fears, deteriorating fundamentals and distressed funds slowly selling down their stake (GTX emerged from bankruptcy in 2021).

The company seems to be doing well with the cards they’re dealt, but we need a recovery in car volume (or meaningful profits from new areas) for the narrative to turn.

18. Inchcape (INCH.L)

Global car distribution company, now a pure-play after exiting UK retail operations earlier in 2024. This is what they said at the time:

“Transaction consistent with Inchcape's strategic focus on higher margin, capital-light, cash generative, diversified, scalable and global Distribution business. Following the disposal, Inchcape will substantially be a Distribution-focussed business”

They used some of these proceeds to do a modest buyback. Mid 2024 they increased the buyback authorizition. I hope they got a taste for it and will keep buying back shares in 2025.

Currently trading at 11x NTM P/E, on estimates that have come down throughout 2024. 10% EPS CAGR expected in 2025 & 2026

Here’s a recent write-up over on VIC

19. Verallia (VRLA.PA)

Leading European glass packaging producer, facing earnings pressure after a strong 2023.

Verallia has been my worst performer (-32%) in 2024, despite the the NTM EV/EBITDA & P/E multiples staying about the same. This happens when earnings estimates come down, a lot.

Historically this sector has been a stable +2% p.a. growth in sales. But COVID, supply chain issues and destocking afterwards really messed up a lot of companies, including this one. They pushed prices hard and reaped the rewards in 2023, only to get hit in 2024 by a massive slowdown. They claim recovery in demand is confirmed, but slower than expected.

This is a position I’m not entirely happy with. I feel like I should either buy the dip and cut and move on, but I don’t really love either option. Hence I’m just letting my current position ride

Closing Thoughts

I try to build a portfolio, not just a collection of stocks that all happen to be correlated. Having less correlated holdings allows me to sell one stock and take advantage of dips in another that’s been hit harder. While my approach isn’t an exact science, I hope it at least adds some value.

I’ve noticed some recurring themes in the types of stocks I’m drawn to. If you have suggestions that align with these, I’d love to hear them:

Classic cheapness (low P/E) has to be paired with significant buybacks. Value might be its own catalyst in the long run, but ain’t nobody got time for that. (AerCap, Garrett Motion)

FCF inflection points: e.g. the company had limited FCF the past year(s), but is now coming off an elevated capex cycle and reaping the rewards with skyrocketing FCF (Millicom, Caesar’s)

Improving capital allocation: Solid capital allocation is great, but often already reflected in the stock price. The outsized returns typically come when a company shifts from poor or mediocre to decent capital allocation (Bekaert)

First buyback or shareholder-return inflection: Announcement of a first buyback program in years or transition from debt paydown to meaningful shareholder returns (Strathcona, Linamar, Millicom)

Underappreciated business transformation: Businesses that have fundamentally changed the quality of their operations through transformation but remain overlooked by the market (Mattr, Inchcape)

excellent writeup.

Let me try 2, not pushback, but alternative ideas.

On AER, why not AL? newer fleet, smaller size but large enough to hold on its own. Slightly less shareholder-friendly capital allocation, but comped by much lower P/TBV.

On CZR, why not MGM? comparable valuation, equal or higher quality assets, especially regional, stronger digital assets, a much better run biz historically.

Cheers,

I know changing your mind can be painful. Would you initiate a new position? This frame makes it easier sometimes.

I did look at both and liked VID better. I did however not feel comfortable with predicting the cycle in the industry and did not buy VID. The reason I liked VID better was it's low leverage which will allow it to overcome the downswing in the cycle easier.