Portfolio Spotlight: Bekaert

Elevated quality at 7x P/E

Quick Pitch

Bekaert is a boring European industrial with a boring, but solid, setup: a revamped management team disciplined capital allocation, and resilient fundamentals. It trades at just 7.2x unadjusted earnings with a 5.7% dividend yield and a 5.5% buyback yield.

Upside levers include:

Organic growth from end-market recovery and growth investments

Inorganic growth through accretive M&A

A re-rating as the market begins to recognize structural improvements in margins and returns

But even without that, you should do just fine.

Disclaimer: This content is for educational and entertainment purposes only and is not intended as financial advice. Perform your own research and consult a qualified financial advisor. The author may hold positions in the discussed stocks. This is not a recommendation to buy or sell securities.

Intro

Before I stumbled upon Alex Sweet ‘s write-up (“Elevated quality at 8.2x P/E”) on Bekaert from May 2024, I had it pegged as an overlevered cyclical shitco and never gave it an actual second look.

It’s an excellent article that goes deep. The key is that Bekaert isn’t the same company it was five years ago. And the market still hasn’t caught on.

I don’t want to repeat too many things he already wrote, but I’ll just copy his intro that summarizes very well why Bekaert is interesting right now:

Bekaert is a world leader in converting steel into all kinds of wire, cord and rope products.

This is a less acutely horrible business than it sounds. Compared to primary steelmakers, Bekaert is not as capital-intensive, and is far less beholden to commodity price cycles.

Instead, for decades Bekaert suffered from the typical chronic ailments of many family-controlled European industrial firms. High costs, low margins, lack of growth and weak capital allocation made for an unappetising investment proposition.

Radical change came in 2019. Baron Bert De Graeve handed over the chairmanship to outsider Jürgen Tinggren, former CEO of Swiss elevator giant Schindler. Tinggren quickly changed the entire executive team, bringing in a former Schindler colleague as COO and then CEO.

The new team cut costs, set clear new priorities, and delivered much better margins and free cash flow, plus a credible platform for future growth. Bekaert’s balance sheet is stronger now than any time this century. Yet the stock remains dirt cheap.

New management has a focus on ROCE and FCF generation, shifting focus to higher-growth, higher-margin segments. They’re actively pruning low-margin and subscale assets from their portfolio. This seems to be working as they kept the EBIT-margin near 9% in 2024 despite a -9% drop in revenue.

They also used the 2021–2022 commodity windfall to slash leverage from over 2x to just 0.5x and initiated buybacks for the first time.

In my opinion, the stock remains cheap because of three overhangs:

its spotty history,

skepticism about sustaining margins,

and lingering cyclicality with weak end markets.

But fundamentally, little has changed since Sweet Stocks’ original write-up. Except the stock is now 20% cheaper. This is now “elevated quality at 7x P/E.”

Financial Snapshot

2024 Results

Revenue: €4.0 billion (–8.6% YoY)

EBITDAu: €520 million (–7.3%)

EBITu: €348 million (–10.3%), with an EBITu margin of 8.8% (vs. 9.0% in FY2023)

EPS: €4.56 (–4% YoY); EPSu: €5.55 (–4% YoY)

At a share price of €33.45, that equates to 7.3x reported P/E and just 6x on an adjusted basis.

Shares outstanding: 52.7 million → Market cap: €1.8 billion

Net debt (Q4 2024): €283 million, leading to leverage of 0.54x

2025 Outlook

Initially guided for flat revenue and at least stable EBIT margins (Feb 2025). Three months later, this was subtly downgraded to flat revenue and stable EBIT margins.

What’s up with EPSu, EBITu, … ?

EPSu and EBITu refer to underlying or adjusted figures. They exclude one-off items like restructuring charges. I’m not a fan. Bekaert has booked restructuring costs of over €40 million in both 2023 and 2024, with more initiatives coming in 2025. When they recur every year, are they really one-off?

That said, the stock is still cheap on unadjusted numbers. True earnings power likely sits somewhere between reported and adjusted numbers, but EPSu possiby inflates reality: it’s more than 20% above the actual EPS.

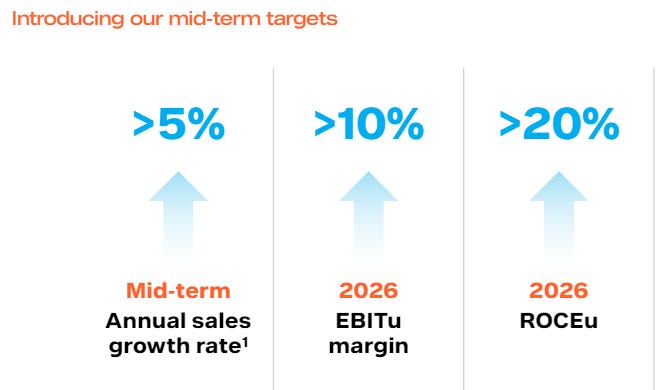

CMD 2023 & Mid-Term Targets

At their December 2023 Capital Markets Day, Bekaert laid out mid-term targets aimed at 2026. With that horizon now approaching, it’s still unclear whether they’ll fully deliver.

But hitting those targets isn’t essential for a good investment result. They’re the cherry on top. What really matters is whether this time is different.

Bekaert talked about a “fundamental and sustainable improvement in margin and portfolio mix,” but so far, the market isn’t convinced.

(Note that they are making disposals of less desirable assets at a premium of where they trade themselves!)

Capital Allocation

Debt level at 0.5x. Targeting a range of 0.5-1.5x net debt to EBITDA. Underlevered right now, holding firepower for M&A. Could temporarily go up to 2.5x for the right deal.

Dividend: progressive dividend policy. I don’t love this especially with 30% WHT in Belgium, but that’s what you get with “family holder” who needs to be able to put food on the table.

Buybacks: were paused in 2024 to prioritize M&A, which was disappointing. But later that year, they announced a €200 million two-year buyback (~5.5% annualized). This showed discipline: they didn’t overpay for deals and instead used excess cash to retire cheap stock. This is how capital allocation should work: flexible with buybacks just one of the tools in the toolbox.

M&A remains on the agenda. Despite active searching, no acquisitions were made in 2024, reflecting discipline on both deal quality and pricing. On the Q1 2025 call, they noted target valuations are coming down, making a 2025 deal more likely. Any acquisition would be funded through internal cash and debt.

Tariffs

Ever since Liberation Day, you can’t talk about an industrial without mentioning the tariff impact. Luckily Bekaert should be able to do just fine, because of its global presence.

Roughly 70% of U.S. sales are produced domestically, with 65% of raw materials sourced locally. The company also maintains flexibility in sourcing and production locations, which helps mitigate direct impacts.

Still, they’re not immune. Broader tariff uncertainty could ripple through end markets and demand.

What could make the Stock Go Up

A common pushback I read about the stock “yes it’s cheap, but you shouldn’t be in a hurry to buy. 2025 is still stable revenue and stable margins, H1 25 will still be weak.”

A simple base case is 5.7% dividend yield + 5.5% YoY EPS growth from buybacks = 11% annual returns, before additional upside from:

return to (organic) growth,

accretive M&A (creating inorganic growth)

multiple expansion (going from 7x to 9-10x P/E isn’t a stretch) on improved fundamentals

confirmation/belief of the ongoing business transformation with higher margins, ROE and growth

This fits my usual framework: it’s cheap now, not overearning, and has clear upside potential.

Bonus: CEO Interview - 13 March 2025

A Belgian financial newspaper had an interview with the CEO a couple of months ago. I provided an English summary in case you want to dig a bit deeper into the company.

1. Investment case and competitive edge

Q. Why should an investor consider Bekaert?

A. The share offers an attractive cash yield: the current gross dividend stands at 5.7 percent and the board follows a progressive dividend policy. In addition, a €200 million share‑buy‑back is under way, taking total cash returns over the past five years to about €750 million.

Equally important, the company has improved its underlying performance. Rising free cash flow is being reinvested in forward‑looking markets—mobility, the energy transition and green construction—while an annual R&D budget of roughly €70 million supports leadership in several global niches.

Q. What sets Bekaert apart from its peers?

A. Its production and sales footprint spans every major region, allowing the group to serve customers locally while retaining global scale. Innovation is usually carried out jointly with customers, a “Better Together” approach that shortens development cycles and deepens relationships.

2. Cyclicality, margins and growth

Q. Many investors still see Bekaert as a cyclical business. Is that fair?

A. Less than it used to be. In recent years the group has maintained an operating margin of 9–10 % despite volatile end‑markets, thanks to disciplined portfolio management. Mature activities such as certain Latin‑American wire plants have been sold, freeing up capital for higher‑growth platforms.

Q. Will the 10% EBIT target for 2026 be met?

A. End‑market demand looks middling rather than buoyant, yet a gradual recovery, coupled with growth drivers like Dramix® concrete fibres, hydrogen components and cable‑reinforcement materials, should help the group reach the goal when the economic cycle turns more supportive.

3. Market backdrop and risks

Weakness is most visible in the automotive supply chain, while construction has cooled in Europe and the United States. China and India, by contrast, remain reasonably resilient.

4. Capital allocation and balance‑sheet capacity

Q. How do you think about deploying capital?

A. Around €200 million a year is earmarked for maintenance and expansion of the existing footprint. Bolt‑on acquisitions in the €50–200 million range will be pursued where the price is right; rich valuations have delayed some deals, but the recent market slowdown is bringing targets within reach. Progressive dividends of roughly €80–90 million a year remain the backbone of the policy, and buy‑backs are executed when they create value.

Q. How much leverage are you comfortable with?

A. The preferred range is 0.5–1.5 times net debt to EBITDA, with temporary excursions up to 2.5 times for exceptional opportunities. That leaves ample room to invest, distribute cash and acquire.

5. Competition and valuation

There is no single company that mirrors Bekaert’s entire portfolio. In tyre reinforcement the main competitors are Chinese and Korean players that currently trade above 10x EBITDA. The group itself changes hands at only three to four times EBITDA; on a sum‑of‑the‑parts basis, applying standard multiples would imply an equity value of four to five billion euros, roughly double today’s market capitalisation.

With the Bekaert family holding more than 35 percent of the shares, a takeover seems unlikely; management prefers to be a consolidator rather than a target.

(Note: I don’t really see the comps trading at 10x EBITDA, but they do trade higher than Bekaert)

6. Macro and geopolitics

Tariff moves such as those recently threatened by the United States have a limited effect because two‑thirds of production is local to the customer base and the group can flex imports as required. A recession in the US would be felt, yet the breadth of the portfolio and global footprint should soften the blow.

7. Segment outlook

Replacement tyres account for the bulk of tyre‑cord demand and provide a relatively stable base, while growth opportunities are strongest in China and India. In green hydrogen the market has moved from hype to more realistic economics, pushing some projects back by one to two years, but the long‑term potential remains intact.

8. Portfolio evolution over the next five years

Management intends to divest activities that lack growth or scale, even if they are profitable, and to channel resources into both organic and inorganic expansion—possibly beyond steel—aiming to translate innovation into global leadership.

9. Share performance and governance

Although the current share price looks low, management’s priorities are investment in growth and a progressive dividend before any new repurchase programme. Liquidity should improve as operational performance and investor communication continue to strengthen. The CEO holds shares personally, and executives are required to build and maintain a minimum position.

welcome back!

am i hallucinating some similarities with lanxess in both industry and journey?

Thanks, looks like a very interesting name.