Portfolio Spotlight: Millicom

Ready to finally generate significant FCF. Monetization of the towers adds some extra "oomph" to the thesis.

Quick Pitch

Stock left for dead after compelling investment pitch turned sour and Cable Cowboy CEO disappointed investors.

French telecom titan rapidly acquired a 30% stake in 2023 and put some of his guys on the board. Current CEO will leave mid 2024.

With elevated capex behind them, combined with cost savings, the company will finally generate substantial FCF: it has a projected NTM FCF yield of 16.2%

Bonus: monetization of their tower assets, which could be a significant catalyst in accelerating into debt paydown and buybacks

Disclaimer: This content is for educational and entertainment purposes only and is not intended as financial advice. Perform your own research and consult a qualified financial advisor. The author may hold positions in the discussed stocks. This is not a recommendation to buy or sell securities.

Intro

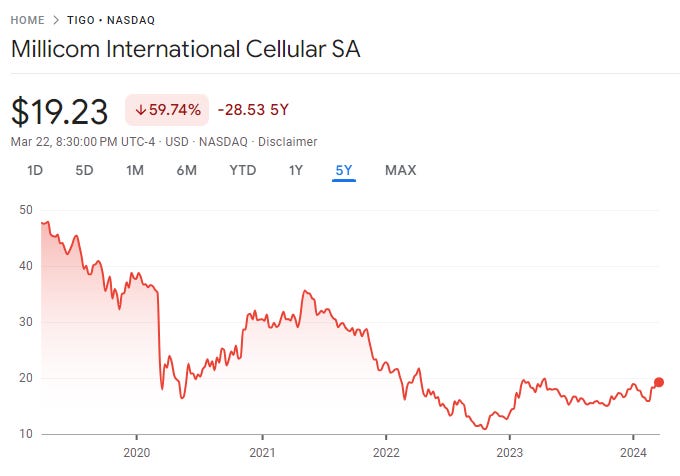

Believe it or not, a few years ago “The Charter CHTR 0.00%↑ of Latin America” was considered a compelling investment pitch. This was mostly true before August 2021, which marked the top of this concerning chart pattern.

Millicom is a Latin American telecom company. It generates over half of its profits in Guatemala and Colombia, but it also operates in several other countries1.

The current CEO, Mauricio Ramos, comes from the “church of Malone” and sits on Charter’s board. Unfortunately, it seems like he lacked the magic touch to make the stock go up (maybe in combination with being dealt a bad hand).

Shareholders have been waiting for buybacks, but this didn’t materialize until very recently. Instead, in 2022, Millicom acquired the part of the Guatemala JV they didn’t own at 6x EBITDA, while conducting a rights offering at 4x EBITDA. Although intrinsic value is about more than EBITDA multiples, issuing shares at 4x to buy shares at 6x does not sound very outsider like.

The stock was already in a downtrend and this transaction really killed the story for many investors.

So why care now?

Valuation

Millicom trades in the US as TIGO 0.00%↑ , but there is more liquidity in the Swedish listing. With 171.5 million shares outstanding and a current share price of $19.8, the market cap is about $3.4B. Like many telecom companies, Millicom has significant debt. Including leases, net debt is about $7B2, leading to an Enterprise Value (EV) of $10.4B.

For FY 2023, EBITDA was $2.1B. This is lower than 2022 due to some one-offs, but estimates for 2024 are almost $2.4B. This results in a last twelve months (LTM) ratio of 3.3x EBITDA to net debt—a manageable level, with further deleveraging planned.

LTM EV/EBITDA is 4.95x.

NTM EV/EBITDA is 4.32x

But the stock has always been cheap on EV/EBITDA basis, so why care now?

The problem with cheap on an EBITDA-basis is that it doesn’t necessarily translate into FCF. Luckily for us, that’s about to change for Millicom. After substantial capex spend in 2023 and succesful cost-saving measures, the company projects generating significant FCF in 2024: $550m. The CEO called this a sustainable number that can be grown.

That would be a P/FCF of 6.2x, or a FCF yield of 16.2%

As you can see on this slide, there hasn’t been much FCF in the past 2 years. So it’s really about what will be generated in the future. If plans unfold as expected, we’re at an inflection point not yet reflected in LTM numbers.

I’d say that’s a pretty good first reason to care now.

Monetization of the Towers

On top of this juicy FCF yield, Millicom owns some valuable assets they’re in the process of monetizing, e.g. through a sale-leaseback or selling a partial stake to an outside investor.

A key asset is their collection of over 10,000 towers, now put into a separate TowerCo entitiy, Lati, which management is actively trying to monetize. It’s not yet clear if they well sell a partial stake, or opt for a complete sale-leaseback. This process has been ongoing for a while and should reach its conclusion soon (it was actually planned to be done by Q4 23)

Estimates for the potential value of the full TowerCo have been between $1B - $1.5B (equivalent to $5.8 - $8.7 per share). But not all towers are created equally and interest rates have changed since the initial estimates were released. Nevertheless, $1B seems pretty realistic based on what I have read.

During a November 2022 analyst call, the CEO said that a sale-leaseback would be EBITDA neutral. This is because Millicom's current annual investment in tower capex would be replaced by lease payments to the TowerCo. (But it’s not a problem if this transaction ends up being not 100% EBITDA neutral)

Separating the towers will be EBITDA neutral to Millicom, but the towers separately fetch a much higher multiple than the base telco operator business. Thus, in a bit of financial engineering magic, you conjure up value out of thin air without impairing the company’s earnings and debt servicing capacity.

It almost sounds to good to be true, but telecom companies who still own their towers have an opportunity to generate value through multiple arbitrage. Towers outside of a telco are just more valuable to an external investor, or the market. 3

However, divesting these assets creates greater operating leverage into the business. A sale-leaseback transaction transforms these fixed assets into cash but this introduces operating expenses in the form of lease payments.

In a potential downturn, you still have to make your lease payments. Owning the tower assets on the other hand, would offer the flexibility to reduce capital expenditures on tower maintenance or expansion.

The pending towers-deal is a second reason to care now. Freeing up this cash can accelerate debt paydown and significant share buybacks.

FY 2023 Results

After mediocre results and careful outlooks throughout 2023, Q4 results brought a notable shift towards optimism about the future. Here are some direct and paraphrased quotes from the conference call:

Right now we focus on making $550m FCF reality in 2024, and we will give future guidance for 2025+ later... but $550m is a sustainable number that can be grown

Different markets are under control and an have improved outlook.

Cost savings plan has been succesful and we have expanded it.

We've now seen the worst of the spectrum renewals and spectrum costs. Going forward, we see more normalized spectrum spend.

Looking forward to monetization of Lati (the TowerCo)

When you put it all together: increased margins and sustained profitability.

Xavier Niel

Despite the improved outlook, investors are still wary of Millicom and its management. A shift in leadership could be the final piece of the puzzle.4

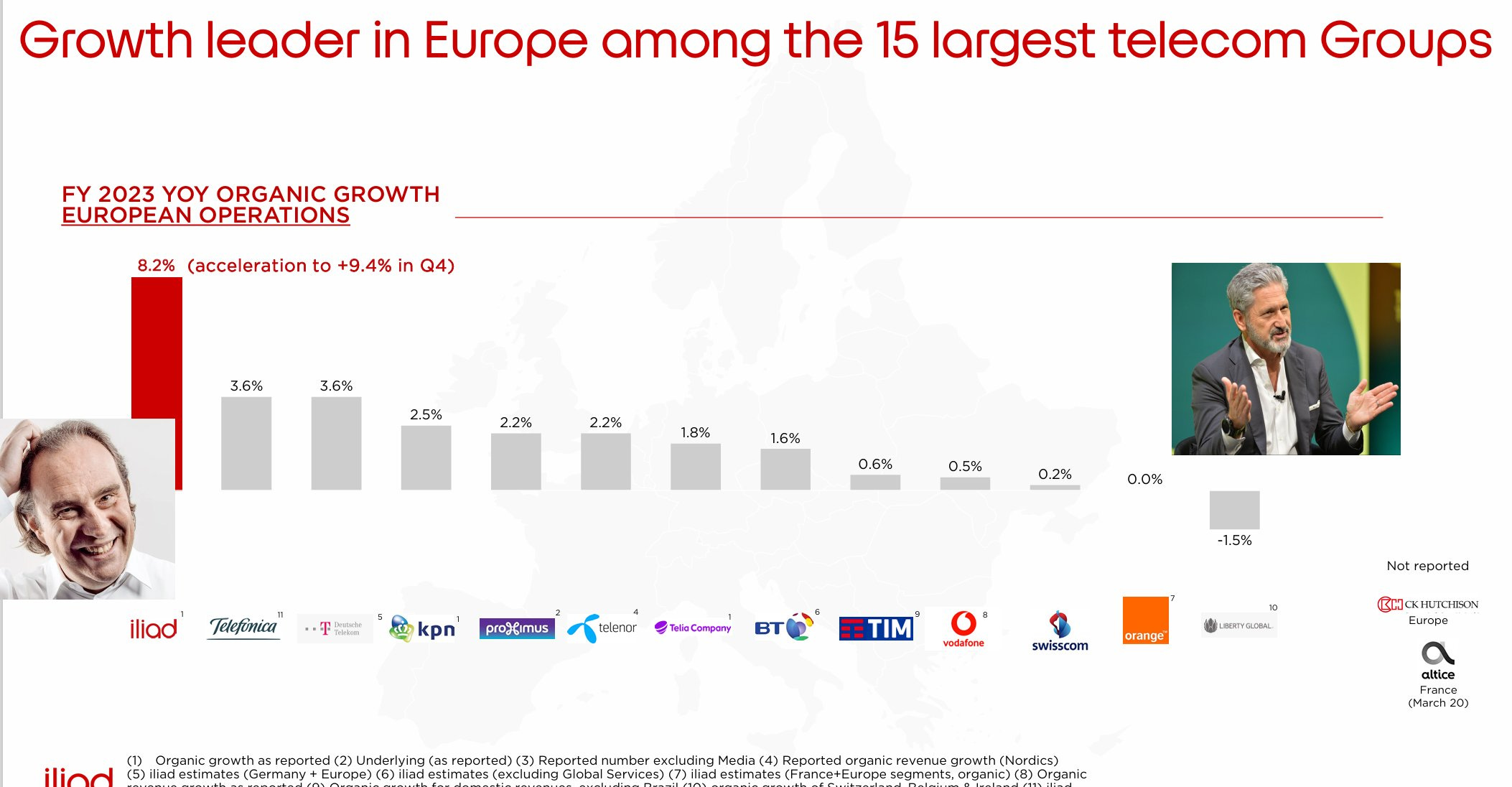

Xavier Niel (XN) is a French billionaire probably most known for owning the low cost telecom provider Iliad, whose organic growth of 8% outpaced its European peers in 2023.

He popped up as a new Millicom shareholder with a 7% stake in November 2022. By mid-February 2023, he filed for a 19.6% stake. He kept buying on the open market, paying as much as $20.8 per share, up to an almost 25% stake right before the AGM on 31/5/23. He got a couple of his representatives on the board of directors. In September 2023 Maxime Lombardini, the former CEO of Iliad, became the COO of Millicom.

Right now Xavier’s stake is right below the 30% threshold. Going over that would force him to make a mandatory offer for the whole company.

Needles to say, Niel’s grip on Millicom is strengthening, but I think we as minority shareholders should be happy about that. His general strategy is:

Cut costs

Monetize infrastructure

Use proceeds for dividends or buybacks if the stock is cheap

It’s not his first rodeo and he has successfully used this exact strategy in past ventures. Check out this twitter thread for the story about him taking private Irish telco Eir.

Last year it wasn’t clear what has plan for the company was. And it still isn’t. What does this rapid accumalation of shares mean? Is he going to make a takeover offer any time soon? If he does, he would likely try to frontrun the tower transaction, to capture the full value of that himself.

But the upbeat outlook on the Q4 23 call showed to me that right now he’s simply a big shareholder ready to share some of value with minority shareholders. This of course can always change in the future.

One interesting titbit mentioned by

is that XN never stated he did not want to buy all of Millicom.The absence of saying he wouldn't buy all of Tigo for 1.5 years means that he has wanted to keep the possibility open throughout that time.

There is nothing accidental about what is communicated, or not, to the market in these cases. In Tele2, in Vodafone, and in Unibail he has said that they are not aiming for the entire asset but not here.

(Personally I got interested in Millicom thanks to the extensive coverage of

. In this post, he paints the initial picture at the start of 2023:His substack covers all the developments in detail. It’s a nice diary of the developing saga, with the info that was available at the time. The comment section is also a useful source of info!)

My Transactions in the Stock

I first bought a stake in TIGO 0.00%↑ early 2023 as kind of a shorter term special situation, trying to frontrun a potential takeover bid (Apollo was also rumoured to be interested back then) or tower monetization.

Over time, my investment thesis has evolved. There still is the special situation angle of the tower monetization, but I am not hoping for a takeover bid anymore. I’m fine holding onto the asset and let a capable operator work his magic.

Following the FY23 results announced at the end of February, I increased my stake both in the model portfolio and in my PA. The outlook was so positive that the stock seemed to be a better deal than before, even after being up 10% that day.

Modest Bull Case

I stumbled upon an interesting Swedish tweet thread that showed how even with a relatively modest bull case, the stock price can really skyrocket.

I have rephrased it a bit in a way that makes more sense to me:

We’ll look at a 3-year CAGR. The current EV/EBITDA multiple is 4.3x, let’s start with assuming both the EBITDA and the multiple stay flat. Cash generated nullifies debt in the EV calculation, meaning market cap must go up to keep the EV constant.

From FCF generation alone, $550m annually and $1650m in 3 years, the market cap would rise from $3.4B to $5.05B, resulting in a 14.1% CAGR

A sale-leaseback of the towers, assuming $1B proceeds spread out over 3 years: market cap goes from $3.4 to $4.4B = 9% CAGR

When combining these two, the market cap goes from $3.4B to $6.05B based on $2.65B cash generated = 21.2% CAGR

If you add some EBITDA growth or multiple expansion:

Annual EBITDA growth of 5% with a constant multiple is 5% CAGR for the EV. This is a 14% CAGR for the equity.

The EBITDA multiple expanding from 4.3x to 5x is another 5.2% CAGR over 3 years. Again, more than 14% CAGR for the equity.

If you combine all of these, the projected CAGR over 3 years is more than 40%.

And in practice, if Millicom reaches 5% EBITDA growth, it’s reasonable to expect FCF to also grow. On top of that, the EBITDA multiple could always go higher than 5x. In our simple calculation above, generated cash is used to reduce debt. But it can easily be allocated in ways that generate higher returns.

That’s why I think this is still a modest bull case. The assumptions aren’t overly optimistic and the stock will still be cheap even after 3 years of 40% CAGR.

Why Does the Opportunity Exist?

Telecom investment pitches have lost some of their appeal

Company has been cheap on EBITDA basis for ages

Plenty of investors have lost money on the stock and have given up

FCF generation in 2022 and 2023 sucked. EBITDA in 2023 is lower than 2022.

Lati monetization has dragged on and company can’t comment much on the ongoing process.

Need some faith in the new operators and their outlook. It’s about the future FCF generation. Not about the past.

Conclusion: Why Now?

Not just cheap based on an EBITDA multiple, but on actual FCF generation

Monetization of towers

New aligned insider who not only understands the industry but also has a proven track record of success

Resources

glimourk on twitter and his alwaysinvert substack has been my main source of info for everything Millicom.

There’s a thread on CoFB. Mosts posts are from before 2021. gilmourkh/alwaysinvert occasionally provides a bullish update but no one cares anymore. I love it.

Personal Update & Looking Ahead

I publish the trades I make in the model portfolio live on Substack Notes. I’ll likely do a quarterly “fund letter” or returns analysis.

I wanted to start a model portfolio at the beginning of 2024 and so I did. However, I also became a father around the same time. Let’s say I was a bit too optimistic regarding my writing output under these circumstances :)

The pace of writing has been slower than initially planned, and I’m still trying to figure out what I exactly want to write about.

But I’m happy with the feedback and subscriber growth so far. If you’ve enjoyed my work and want to encourage me to write more, the best way to do so is by interacting with my posts: like, comment or share with someone who might enjoy it.

Panama, Paraguay, Bolivia, El Salvador, Nicaragua and Honduras

Millicom, like other telcos, actually focuses on EBITDAaL (EBITDA after leases), and net debt, ex leases.

LTM EBITDAaL is $1.8B, net debt $5.95B. => net debt / EBITDAaL of 3.3x. They plan to reach 2.5x leverage ratio measured like this by 2025, through debt paydown and EBITDA growth

Every tower has tenants: telecom companies that lease space on the tower. A pure play TowerCo can easily serve multiple tenants (= increase the tenancy ratio) and thus get value out of every single tower. The TowerCo also has access to cheaper debt.

For me it was actualy the first piece: because of XN’s involvement, I started reading more about Millicom and invested in it in 2023.

I linked to your post in my post for today - Emerging Market Links + The Week Ahead (April 1, 2024) https://emergingmarketskeptic.substack.com/p/emerging-markets-week-april-1-2024

The The Bonhoeffer Fund’s Q1 2023 Partner Letter and Q4 2022 Partner Letter and maybe others have discussed the special situation there in some detail... Not sure if more recent letters have covered the stock as they are or were investors in it...