Q3 2024 Portfolio Review

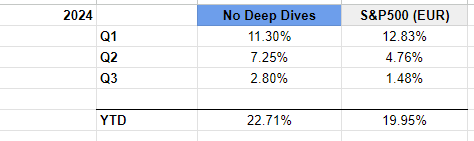

Up 2.8% in Q3 24, 22.7% YTD

I. Results

Q3 2024 Returns

No Deep Dives Portfolio: +2.8%

S&P 500 (in EUR): +1.5%

YTD Returns

This brings year-to-date results to 22.71%

Portfolio at the end of Q3

Some big winners were Bel Fuse (BELFB 0.00%↑ ) and Caesar’s (CZR 0.00%↑) . The biggest loser by far, was Verallia.

II. Portfolio Updates

Top Detractor(s)

Verallia (VRLA.PA)

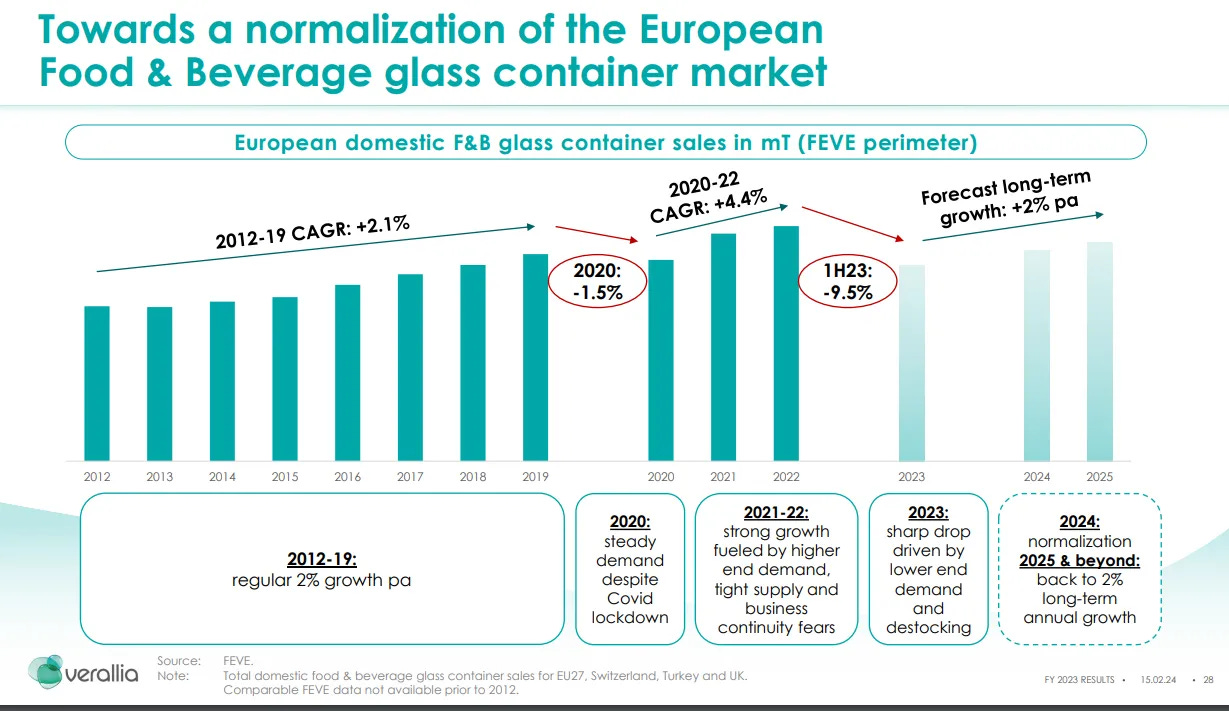

Verallia took a significant hit after reducing its guidance ahead of earnings and dropped further following the actual H1 2024 results. The share price fell from €34 to €26 (-23.5%) in just a few weeks.

Back in April, I discussed their Q1 2024 earnings:

At the time, the key point for me was that Verallia confirmed seeing a rebound and reiterated their €1B EBITDA goal for 2024.

“Verallia started the year in line with expectations, with lower activity and prices compared to Q1 2023 which set a high basis of comparison. As expected, we are seeing encouraging signs of recovery from the Q4 2023 low. The continued commitment of our teams and the impact of the Performance Action Plan have enabled us to post a sequentially improving performance in the current market context.

We confirm our guidance of an adjusted EBITDA of around €1 billion in 2024, with performance gradually improving over the course of the year”

So, it was a surprise to me—and the market—when, less than three months later, Verallia issued a profit warning, cutting its EBITDA guidance to about €866m (“around the same level as 2022”).

Initially, I lazily assumed 2024 EPS would be similar to 2022's (€2.92). However, someone on Twitter rightly pointed out that higher D&A and finance costs in 2024 would result in a lower EPS for the same EBITDA.

(operating leverage on the way up: 😄

operating leverage on the way down: 😭)

Analyst estimates currently are as follows:

So at a share price of €25.3, the stock appears cheap even with the reduced outlook. However, I suspect the market is shook by the sudden shift in guidance and perhaps concerned about the unpredictability in the covid aftermath for an industry that was traditionally seen as pretty stable.

I suppose I’m also a bit shook by the events and uncertainty. Instead of adding to it like I often would, I simply kept the position I already have.

Top Contributors

Bel Fuse (BELFB)

Bel Fuse ( BELFB 0.00%↑ ) reacted positively to its Q2 24 earnings and the stock went from $66 to $75. I took that opportunity to trim the position. While the Q2 results exceeded expectations, the outlook remained lackluster, with no return to sales growth. This felt similar to the setup that caused the stock to crater earlier in the year, as I discussed here

Some turbulence in the market brought the stock back down, but on September 19th, Bel Fuse announced the acquisition of Enercon. The stock shot up by over 10%, closing the day above $80.

The Good:

Enercon is a pure play in defense and aerospace, sectors with faster growth and higher margins.

Bel Fuse put its underleveraged balance sheet to use, bringing debt to 2x EBITDA.

The Bad:

40% of Enercon’s revenue and its HQ are in Israel. Given the “elevated geopolitical unrest,” this could be concerning.

The acquisition came from Fortissimo Capital, a Tel Aviv-based PE firm. Was this a "forced" sale due to fund winding down (good for BELFB), or just monetizing an investment at a favorable price (less ideal for BELFB)?

The acquisition price of 10.5x EV/2024 EBITDA is higher than Bel Fuse’s own valuation, but this may reflect a higher quality business with better growth prospects. However, it would be nice to see a return to organic growth in Bel Fuse’s existing operations as well.

Caesars Entertainment (CZR)

Caesars Entertainment, a.k.a. Caesar’s ( CZR 0.00%↑ ) jumped 8%+ on their Q2 24 results. As a reminder, CZR operates 3 segments: Las Vegas, Regionals and Digital. While Vegas and Regionals were largely in line with expectations, Digital was the standout. Digital revenue increased by 30%, with 50% of that flowing through to EBITDA.

The Digital segment is now on track to deliver $200 million in EBITDA this year, and management reaffirmed its target of reaching a $500 million EBITDA run rate by 2025. CEO Tom Reeg has been stating this goal for a while:

“… and that's how we get to the same $500 million we've been talking about for 3 years now. You'll believe it at some point.”

On top of that, CZR expects a strong H2 2024, with continued momentum into 2025:

“Rest of the year looks strong. Expect Vegas to post growth. I know that that's not what's been reflected in estimates, but we feel very good about the rest of the year and into '25.

We have with we've not seen a lot of elasticity when it comes to pricing in Vegas. So we have continued to take price kind of across the board, not just rooms, restaurants, ATM fees, pool cabanas. There's just a massive amount of demand for Vegas and that has continued.”

For a long time, CZR has been a "show me" story, with the CEO more bullish than analysts and the market. Now, with the Digital segment inflecting and share buybacks beginning, it seems the "showing" has started.

For more background, check out my brief introduction when I first added CZR to the model portfolio.

Other Notable Portfolio Updates

Millicom (TIGO)

Lots of thing happening with Millicom ( TIGO 0.00%↑ ). To get you up to speed, I will refer you to my substack post here:

After that post, and just before earnings, Xavier Niel (XN) raised his offer from $24 to $25.75. However, Millicom’s independent committee still recommended rejecting the increased offer.

They argue it undervalues Millicom among other things because it's a 33% discount to the valuation of the peer group, based on FCF yield

=> an offer in line with the FCF yield of the peers would be about $39

And that’s still without taking into account growth prospects & outlook, value from potential M&A and value from a tower monetization.

To me, it seems like the independent committee is saying $39 would be the minimum offer in order to start considering accepting it.

XN did manage to scoop up about 10% of Millicom’s shares, raising his stake from 30% to 40%. Some "bumpitrage" traders likely saw a quick profit at $24 and took advantage.

What’s next? No one knows, but

tries:AerCap (AER) assumes A320neo’s from Spirit Airlines’ order book

AER 0.00%↑ posted good results and increased guidance again. In addition to that, they opportunistically managed to skip the line for some A320neo’s. A pleasant surprise in a world with constrained new airplane production.

“We have agreed to purchase 36 A320neo family aircraft. This transaction results in AerCap assuming 36 aircraft from Spirit's order book and the related pre-delivery payments. ... These aircraft are set to deliver in 2027 and 2028, which match well with the profile of our existing order book and is far sooner than we would otherwise have been able to negotiate directly with Airbus and gives us an opportunity to support a long-term customer simultaneously.

Furthermore, we will also backstop up to 52 A320neo family aircraft in Spirit's order book, if needed. These additional aircraft would deliver from 2029 onwards. This deal takes our total aircraft added this year to over 50, as I am confident there will be similar opportunities for organic growth to come. The smaller number of aircraft delivering into the system as a result of the OEM delays has provided some respite to airlines from a financing perspective, but this will change over time and AerCap is well positioned to take advantage of it.”

Some airlines lack the financial power to purchase all the planes they've ordered, and sale-leasebacks with companies like AerCap become an attractive option. On AerCap’s terms, of course.

Air Lease ( AL 0.00%↑ ) also commented on this trend in their recent earnings call:

Historically, as airlines start to experience any financial squeeze, historically, that is always favored leasing. I do think there's going to be a large opportunity, though. The airlines have definitely over ordered and a lot of them don't have quite the access to capital as we do here as an investment-grade public company. So I think there's going to be a search for financing on behalf of the airlines and there'll be a lot of airlines that will need help.

A gut reaction for many to this deal is: “but what if Spirit goes bankrupt?”

I think AerCap is happy to take over their order book and the good thing about airplanes is that when the customer goes bankrupt, you can just transfer the planes to a new customer.

Exited/Trimmed Positions

Trimmed BELFB 0.00%↑ at $75.3

$NTDOY at $13.53

CACI at $467.2

Trimmed RLGT at $6.5

New/Increased Positions

Added to TIGO 0.00%↑ at $24.5

Added to CZR 0.00%↑ at $35.10

LSXMA 0.00%↑ at $21.95

Added SIRI 0.00%↑ at $23.56

Opened position MC.PA at €658.10, added a bit at €603.6

Added to MACF at 113p

These are all covered in my Substack Notes when I make them, with brief commentary. So have a look over there for more on these transactions.