TT Electronics: Turnaround with Takeover Chatter

Cheap valuation, merger arbitrage upside, and the chance of a higher bid make this a compelling watch

Introduction

Serial underperformer in the midst of a turnaround.

Shares are cheap on normalized metrics.

Merger arbitrage opportunity with an 18% spread.

Potential upside if a competing bidder emerges.

Disclaimer: This content is for educational and entertainment purposes only and is not intended as financial advice. Perform your own research and consult a qualified financial advisor. The author may hold positions in the discussed stocks. This is not a recommendation to buy or sell securities.

Quick History

TT Electronics (TTG.L) is a global designer and manufacturer of electronic components and a turnaround story with a promising new CEO appointed in 2023.1

However, like what can happen with turnarounds, it has been weighed down by recurring ”one time”charges, creating a significant gap between adjusted and unadjusted earnings. Compounding the issue, TTG issued a major profit warning in September, causing shares to plummet by 37%. This was followed by further guidance cuts, narrowing estimates to the lower end of the previous range. Here’s a write-up on Value Investors Club written at that time.

The shares began 2024 at 157p, drifted to 140p before the profit warning, and then plunged to 89p. A month later, they slid further to 79p. Until…

… On November 15, Volex (VLX.L), a larger peer, publicly announced its intention to make an offer for TTG. The proposed deal included 62.9p in cash plus 0.223 Volex shares for each TTG share. At the time, the offer valued TTG shares at 135.5p.

TT Electronics responded later that day, stating that they:

recently received and rejected an all-cash indicative proposal from another party at a significantly higher value than the Volex Proposal

rejected the Volex Proposal as fundamentally undervaluing TT Electronics and its long-term prospects.

Today, Volex released a presentation outlining their case for acquiring TT Electronics.

The short version is: “you suck, we don’t, let us run your business”.

The Chairman addressed the “recently received” all-cash indicative offer, noting that it isn’t a firm alternative for shareholders. It’s possible the offer was made before the significant share price drop in September, meaning the same party might no longer be willing to pay that price.

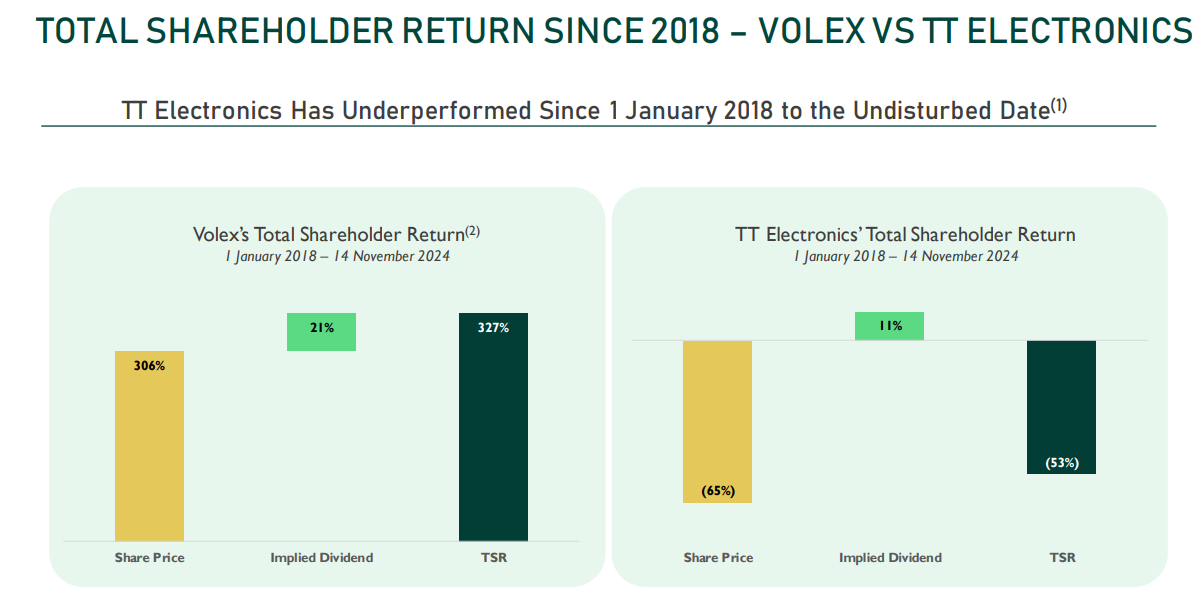

TT Electronics is an attractive acquisition target due to its lack of scale, which could be improved as part of a larger organization. Volex has a strong track record of successfully integrating acquisitions.

You can find that presentation here.

Valuation & the Proposed Deal

At the current price of 106p, TTG shares trade at a “normalized” NTM P/E of 7.5x

So even at an elevated price because of M&A chatter, the shares are still optically cheap... assuming no further negative surprises.

The Volex offer is currently worth 126.7p, representing an 18% premium. Volex has until December 13 to make a firm offer.

TTG shares look appealing if you’re comfortable receiving Volex shares as part of the deal. However, the real kicker is TTG being “in play.” If there are other suitors, which seems plausible, they need to speak now or forever hold their peace.

If not, the Volex offer seems reasonable.

That said, there’s a risk the deal falls through if shareholders reject it. The offer is lower than TTG’s share price at the start of the year, and investors might prefer to give current management more time to execute their turnaround strategy rather than selling out to Volex.

Therefore, a key consideration for potentially investing in TTG shares is: are you comfortable holding them if there is no deal?

Do You Want to Own Volex?

And what about Volex?

At the current price of 289p, it’s trading at 10.6x NTM P/E, below its 5y mean of 13.6x. It’s a successful turnaround, focusing on revenue growth while hitting an operating margin of 9-10%. A serial acquiror with organic growth and a focus on ROCE.

Nat Rothschild, the executive chairman, owns 25.7% of the company through NR Holdings. That’s some serious insider ownership.

Some highlights from their FY24 presentation in June.

What I’m less fond of is a 5y plan like this:

I want a focus on per share metrics, not an absolute revenue target that you could hit by issuing shares and just making acquisitions without paying attention to any “return on capital”-metrics. That said, the fact that they emphasize ROCE in their own presentation is reassuring.

Conclusion

TTG shares currently look interesting to me at first glance, but since I only just started reading up on Volex a couple of days ago… I haven’t pulled the trigger yet.

I’m publishing this post anyway, since I wanna get it out while the news is still fresh. And maybe one of you has a stronger opinion here about standalone TTG, the appeal of Volex and chances of getting a higher offer.

A different post than my previous ones, so don’t hesitate to give me feedback. A like or share goes a long way.

Resources

CEO Peter French joined TT in 10/2023. Previously he was CEO of Rotork for 9 years, and most recently led ASCO through a bank-owned turnaround before selling to PE. (source: https://www.valueinvestorsclub.com/idea/TT_Electronics/6934012669)

Update: Volex will not make an offer "as it is now clear that the Board of TT Electronics is not willing to recommend an offer at a valuation that is also acceptable to Volex."

https://www.londonstockexchange.com/news-article/VLX/statement-re-tt-electronics-plc/16809209

Here's a bit more on Volex Plc from another substack:

https://increasingodds.substack.com/p/volex-plc

https://increasingodds.substack.com/p/volex-plc-update