Digesting Millicom’s Tower Monetization

Sale-leaseback announcement with SBAC leaves TIGO stock unmoved. Clarity on 2025 capital allocation is what investors need now.

Two weeks ago, on October 28th, Millicom ( TIGO 0.00%↑ ) finally announced its long-awaited tower sale. This sale-leaseback of (part of ) the tower portfolio has been anticipated as a potential catalyst for years.

Finally the wait was over, and … the stock basically didn’t move on it. That raises the question: when everyone is expecting a catalyst, does it lose its effect? Priced in?

But instead of zooming in on short-term price movements, maybe we should focus on the bigger picture: what does the company's future look like (good), and is the stock still good value (yes)?

As investor (and not traders), that’s where our focus should lie. However, I always pause when an expected catalyst doesn’t move the needle as anticipated. It’s a reminder to keep my assumptions in check.

Disclaimer: This content is for educational and entertainment purposes only and is not intended as financial advice. Perform your own research and consult a qualified financial advisor. The author may hold positions in the discussed stocks. This is not a recommendation to buy or sell securities.

Why do a Sale-Leaseback?

By selling the towers (TowerCo) in a sale-leaseback transaction (SLB), Millicom:

Gets up front cash

Eliminates operating expenses (opex) associated with TowerCo

Avoids future maintenance and expansion capex for TowerCo

BUT

Does have to pay leasing costs to TowerCo

While you would expect the telco to take a hit in FCF, the upfront cash they receive should generate enough per-share value to make it worth it.

I hate the phrase multiple arbitrage, but that’s what’s going on here. Infrastructure investors and specialized companies such as SBAC 0.00%↑ , pay higher multiples for the telecom towers than the market would pay for a telecom company.

Seperating the infrastructure assets from the parent company unveils and maximizes the value of the NetCo, but it does leave behind a slightly weaker ServCo1

And there’s an easy way to capture the value of this multiple arbitrage: sell assets at a high multiple, then buy back your own shares at a lower multiple.

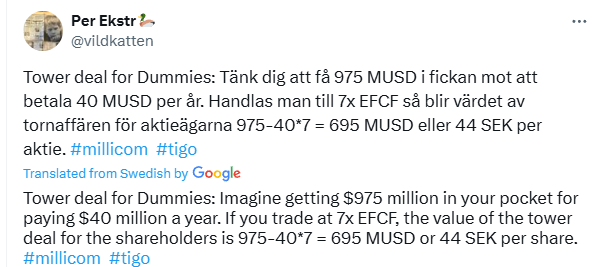

For example, Millicom sells towers for $975 million, with an estimated $40 million hit to annual FCF. If they use $800 million to buy back roughly 30 million shares at $26.50, here's how it would play out:

Before the transaction: $650 million in 2024 FCF, with 171.5 million shares = $3.79 FCF/share

After the transaction: $610 million in FCF, with 141.5 million shares = $4.31 FCF/share

This results in a permanent 13% increase in FCF per share.

Or another way of thinking about it:

It’s not a total free lunch though. The maximize the profit generated by the towers, SBAC will open them up for competitors. This could impact Millicom’s competitive position. And in a downturn, ServCo is locked into lease payments, whereas owning the assets might provide more flexibility to manage costs during tough times.

That said, the upfront benefits should drastically outweigh any potential downsides.

The Deal

The transaction was announced as part of the Q3 24 earnings report for SBAC:

Over 7000 sites sold for approx $975m (+ potential earn-outs)

These are expected to generate approximately $129.0 million of revenues and $89.0 million of tower cash flow during their first full year of operations after closing.

Millicom has entered into 15-year leases for these sites.

Leases in USD, so Millicom carries currency risk. But this should go hand in hand with low yearly escalators.

SBAC is committed to build up to 2500 “build-to-suit” sites and Millicom gets dibs

SBAC revealed some financial details from their perspective:

The headline multiple was 11x “tower cash flow,” equating to approximately 11.5x EBITDA. But this is on the numbers a year after closing. An LTM EBITDA multiple is likely a bit higher. The towers will serve multiple tenants, not just Millicom, with a current “tenancy ratio” of 1.2. The provided figures likely assume a higher ratio, as SBAC should aim to increase tenancy.

SBAC noted the earn-outs are not material and did not provide details on the escalator terms.

Why No Stock Price Reaction?

I can only speculate, but here’s my best guess:

Lower-than-Expected Valuation: Some investors and analysts had hoped for a higher price. In my initial analysis, I mentioned a value of $1-1.5 billion for the full portfolio (10,000+ towers). This was based on older analyses, which seemed reasonable at the time. Rising interest rates didn’t help, so to my untrained eye, the actual price seemed very reasonable.

Note that they haven’t sold all the towers, but they made it clear they aren’t planning to sell the remaining towers anytime soon. More on that later.

Uncertainty About Proceeds: The biggest issue for me was the lack of clarity on how Millicom intends to use the proceeds. If they had announced a special or recurring dividend, tender offer or buybacks, I believe the stock would have seen an immediate boost. But now, the uncertainty remains: “yes, they’ve monetized the towers, but will regular shareholders see the benefit before Xavier Niel swoops in and steals the company?”

Partially Priced In: If the SLB increases the intrinsic value of TIGO 0.00%↑ by around 13%, some of that upside was likely already reflected in the stock price, given that the market knew Millicom was working on tower monetization. While I didn’t expect a full 13% jump on the day of the announcement, I was surprised to see almost no reaction at all.

Incentives of the Majority Owner

Xavier Niel, now through Iliad, currently owns 40% of Millicom, and it's clear pretty clear this is not were the story ends. But he is patient and seems comfortable with building value that may not immediately get reflected in the share price.

Since he’ll likely increase his stake over time, Niel might prefer a lower headline sale price in exchange for favorable lease terms and the build-to-suit agreement. He doesn’t need to drive immediate value through big share buybacks, as he stands to capture more of the created value if he buys additional shares for cheap (some or all of them). He could go for more capex or M&A that generate excellent long term value, but offer nothing to investors who are counting on near term capital returns.

From what I have heard, he’s not known for treating minority shareholders badly. But he doesn’t run a charity either.

Millicom’s Q3 24 Earnings

On Thursday the 7th of November, Millicom reported its Q3 2024 earnings, with solid business performance and a reaffirmed outlook.2 But my focus was on:

More detail on the financial impact of the SLB

Use of the proceeds (buybacks?)

The analysts were wondering the same, and we got more info during the Q&A session of the conference call.

Financial Impact of the Sale-Leaseback (SLB):

EBITDA: The SLB is expected to be neutral at the EBITDA level.

Free Cash Flow: Anticipated annualized net impact on FCF is -$40 million.

Proceeds: The headline figure is $975 million, though taxes and a partner share for towers in Honduras will reduce the net amount. They didn’t want to give an exact number.

Getting (almost) $975m now for taking an annual $40m hit to FCF sounds pretty sweet to me!

Unsold Towers: About 2,500 towers remain unsold, with a significant portion in Bolivia. Due to Bolivia’s economic crisis, selling these isn’t a priority and wouldn’t yield substantial proceeds anyway.

Capital Allocation and Shareholder Returns:

“We wouldn’t do any shareholder remuneration until we get to 2.5x…. I want to see it there before really opening that discussion. “

(Millicom will be below their leverage target of 2.5x next quarter)

But management is aware that they will have a lot of cash coming in soon and need to have a proper capital allocation plan.

The business is on track to generate $650 million of FCF in 2024, with expectations for this to increase in 2025. They have potential big M&A plans in Colombia next year (up to $1bn), but the tower proceeds basically cover that.

At a share price of $26.5, the market cap is about $4.5bn. $650m FCF means a 14.4% FCF yield to work with.

They consider all options:

Organic capex is priority, but they don’t see that going up in 2025

M&A always an option, but no plans right now besides Colombia

Debt target reached

Dividends / buybacks

Millicom has an authorization to buy back up to 10% of shares, but they clarified that they wouldn’t jump into that without an in depth board discussion on capital allocation.

Best case is we get an update next quarter, worst case is we still have to wait until the AGM in May 2025. But it seems that they will not just let the cash sit there. Either they can put it work at an appropriate hurdle rate, or they will return it on some way.

On top of that, as leonardo1452 rightfully pointed out on twitter: as a GROWING telecom company, they could return even more than generated FCF to shareholders. Growing EBITDA while keeping leverage fixed (at let’s say 2.5x) allows for an increase in debt and thus extra cash to work with.

Conclusion

Millicom is executing well while still being extremely cheap. NTM FCF will be $650-700m, which is a 14-15% FCF yield at today’s price of $26.5.

While the tower monetization didn’t deliver the stock pop some (including me) had hoped for, that’s less relevant for investors willing to hold over let’s say at least the next 12 months.

Millicom will hit their debt target by the end of the year, while having a ton of cash coming in to work with. I’m eagerly awaiting any updates on capital allocation, but also expect the stock to be somewhat dead money until then.

Xavier Niel’s involvement could be a double-edged sword. His influence has driven operational improvements, but it’s important to remember that his incentives as a major shareholder may differ slightly from ours as minority shareholders.

I happily continue holding the stock.

Resources

Seperating the infrastructure assets from a telecom company leaves you with a NetCo and a ServCo. Netco manages network infrastructure and operations, ServCo is the customer facing telecom company.

Actually they now officially upgraded their outlook for 2024 FCF from $600m to $650m. But they already unofficially did this when defending vs the tender offer from Xavier Niel. Back then Millicom provided an outlook of $659m FCF for 2024.