Q2 2024 Portfolio Review

Up 7.25% in Q2, 19.3% YTD. 2 exits & 5 new positions

I. Results

In Q2 2024, the model portfolio returned 7.25%, outperforming the S&P 500's 4.76% return (in EUR). This brings our year-to-date (YTD) results to 19.3%.

The MAG7 stocks continue to dominate headlines, at least in my Twitter feed. While I don’t think it’s productive to dwell on this trend, it implication is that the strong performance of these big names masks the mediocre returns of the average stock. As a result, investors without MAG7 (or AI) exposure are likely underperforming the market.

With that in mind, it's particularly satisfying to beat the index with a portfolio that doesn't include any of these prominent stocks.

Here is the composition of the current portfolio (on 5/7/24):

And here are the results per stock:

The biggest winner was Frontier Developments (FDEV) at +38%. This was a new position that I introduced in the Q1 2024 overview.

TIGO 0.00%↑, up 24%, was the second-biggest gainer but contributed the most to portfolio returns due to its large position size, which I increased in the previous quarter.

The biggest losers were Macfarlane (MACF) and Garrett Motion GTX 0.00%↑, down 15% and 10% respectively. MACF released a somewhat disappointing trading update, while Garrett Motion likely suffered from uncertainty in the auto sector, fueled by new tariffs on Chinese car imports and fears of retaliation and escalation.

Disclaimer: This content is for educational and entertainment purposes only and is not intended as financial advice. Perform your own research and consult a qualified financial advisor. The author may hold positions in the discussed stocks. This is not a recommendation to buy or sell securities.

II. Portfolio Updates

Top Contributors and Detractors

Frontier Developments (FDEV)

When I bought in earlier this year, expectations for Frontier Developments were at rock bottom. Modest trading updates essentially stating "FY24 will be a loss, but we won't need to raise equity" were enough to boost the stock price. It’s very illiquid though, so things can go fast… in both directions. However, the short-term downside risk appears to be gone.

In the coming months, FDEV will officially announce the next CMS game1 , based on their own IP, scheduled for release in FY25. After that, there’s a third Jurassic World game scheduled for 2026 (coinciding with the movie release) and another own IP CMS game in 2027.

Currently trading just above 1x P/S, this turnaround still offers significant upside potential if successful. However, as a small video game company, FDEV is heavily reliant on their next major release. While they seem good at their core CMS game niche, the release could always whiff. Given that risk, a stock like this shouldn't be a big position in your portfolio.

Millicom (TIGO)

Millicom has had an excellent year so far, delivering on their outlook and even increasing it.

For reference, I wrote up the stock earlier:

On May 23rd, Bloomberg “leaked” a take private offer leak by the biggest shareholder, Xavier Niel (XN). In the past I was more naive, but nowadays I always assume there are no accidental leaks. Later that day, XN confirmed a potential offer of $24 per share - below the previous day’s closing price.

Because this lowball offer basically has no chance of succeeding, my initial thought was that this might be a genuine leak, with XN not yet ready to make a real bid. Alternatively, it could be a tactic to anchor expectations to the low $24 price before eventually making a higher bid.

gives brief overview of the events in 2024 leading up to this:In anticipation of the official bid, TIGO already stated that $24 per share would undervalue their future prospects, while sneakily increasing guidance from $550m FCF to “over $600m” and projecting a faster than expected debt paydown.

On July 1st, Niel officially launched a $24 bid. We’re now awaiting TIGO 0.00%↑ ‘s formal recommendation regarding this offer.

The saga is still unfolding, and XN's strategy remains unclear. What I do know is that the stock:

is still cheap: $4.2bn mcap at $24.5, with 2024 projected FCF of over $600m

still has the untapped value in the tower assets

has extra optionality in picking up some local assets for cheap (WOM bankruptcy & buying out their partner in Colombia).

Exited Positions

Again a friendy reminder: all my trades are published live on Substack Notes.

Ming Fai ($3828.hk) at 0.67 HKD

There’s nothing wrong with Ming Fai. It remains a very cheap (albeit HK-listed) stock with a fat dividend yield (9-10%), but no catalyst. I don’t mind having these in the portfolio, but I also won’t hesitate to exit the position for better opportunities.

Asbury Automotive (ABG 0.00%↑) at $233

Asbury looks attractive at 7.5 - 8x fwd P/E, but it risks being "dead money" in 2024 - 2025 due to several factors:

elevated capex until 2026

paying down debt in 2024 (= less money for buybacks)

synergies of their latest big acquisition to be only realized after 2024

With existing exposure to GTX 0.00%↑ and the recent addition of Inchcape, I realized my portfolio might be too overweight the auto sector. Currently, I favor GTX (cheaper with an ongoing massive buyback) and INCH (with a catalyst - discussed below). However, I might reconsider if ABG really steps on the buyback pedal.

New Positions

Inchcape (INCH.L) at 725p

I started a position in Inchcape following their announcement of the sale of their UK retail operations (car dealerships) at what appears to be a favorable price. This move essentially completes their transformation into a pure distribution business while also freeing up some capital for share buybacks.

As stated in their announcement:

“Transaction consistent with Inchcape's strategic focus on higher margin, capital-light, cash generative, diversified, scalable and global Distribution business. Following the disposal, Inchcape will substantially be a Distribution-focussed business;”

I'm drawn to stories where management takes proactive steps to improve the business quality (improving ROE/ROIC, margins, … ), especially when these actions aren't immediately recognized by the market.

I've written more extensively about this investment in:

Sigmaroc (SRC.L) at 63.75p

SigmaRoc is an EU aggregates/limestone operator that transformed itself by acquiring the European assets from CRH. CRH sold those because they’re focusing on its US business, while moving the main listing from the UK to the USA. In a world where UK stocks are hated and US ones get all the index money, this is a move that tends to increase the stock price. Anyway, back to SigmaRoc…

The stock appears very cheap, but there's a catch: SigmaRoc is a serial acquirer that consistently directs investors' attention to adjusted EPS. If the numbers were cleaner, I’d consider making this a bigger position.

But this time, after their biggest acquisition to date, they “pinky promise” us that future acquisitions will be limited to smaller tuck-ins, and "one-time" costs will decrease. If true, we should see adjusted figures converge to unadjusted numbers.

You can read an in depth stock pitch on VIC.

IMAX China (1970.HK) at 7.85 HKD

I discovered this idea on Substack:

The investment pitch is pretty straightforward:

The parent company (IMAX) owns 70% of IMAX China.

IMAX 0.00%↑ attempted a take-private deal last year at 10 HKD per share, nearly succeeding but ultimately failing.

They must wait one year before making a new offer.

Recently, the COO/CFO resigned, and the position was eliminated - a potential signal for another take-private attempt?

IMAX (parent) commented this during their Q1 24 earnings call:

“We haven’t made a decision yet what to do. I think it will depend on China’s financial performance, what our liquidity looks like and then how the Chinese shareholders feel.”

While the stock's overall cheapness provides some downside protection, for me this investment is primarily a play on the take-private setup rather than a long-term hold. I admit this is a more speculative position, which is why a small sizing (2%) seems appropriate.

Philip Morris (PM 0.00%↑ ) at $100

I’ve had my eye in Philip Morris for a while as they seem to be well positioned for “smoke-free” nicotine growth.

However, the catalyst for my recent purchase is ZYN selling like wildfire in the US. It’s small part of their overall business, but it’s enough to reignite growth prospects.

Their September 2023 Investor Day outlined the following growth targets:

For that, you’re currently paying a bit over 15x NTM EPS, with a 5.2% dividend yield. As the sole consumer staple in the portfolio, PM 0.00%↑ also serves a unique diversification function.

Caesars Entertainment (CZR 0.00%↑) at $33.60

Caesar’s stock has been absolutely crushed before I bought it, despite insider purchases and overall optimism by the CEO. There appears to be a big gap between management expectations and market forecasts.

Lots of gaming stocks are interesting, but CZR 0.00%↑ stands out because of inflecting FCF generation for 2025-2026+

Key reasons:

Capex cliff by Q4 24 (reduction in currently elevated capex)

Digital segment growing and producing actual earnings

Management has signaled they will start buying back stock once leverage targets are met, expected around Q4 24.

Additional upside potential exists from a sale-leaseback transaction with VICI 0.00%↑which likely happens in 2024. This is not a must to make the stock work, but could alleviate some leverage concerns by the market.

Reasons for recent poor stock performance:

it’s a “show me “ story and Q1 24 was bad

highly levered stocks got hit as rate cut expectations diminished

consumer discretionary concerns: fear for the state of the consumer and the impact of a potential recession

they likely overspent on digital when ramping up, but should be able to reap the rewards now

Given the speculative nature of this position (wide range of outcomes due to high debt), I have sized this small at a 2% allocation.

After my purchase, news broke out that Carl Icahn bought a stake which seemed to established a price floor. He said there’s no activism planned: he just likes the company, stock price and CEO.

For a more in depth analysis, I highly recommend this podcast episode by

:Other Notable Portfolio Events

AerCap hosted their first Capital Markets Day since 2019. The full presentation can be found here. CEO Aengus Kelly was very optimistic about the company’s future and did a good job at explaining why AerCap is in an excellent position to reap the rewards of a short-term tailwinds and long-term secular trends.

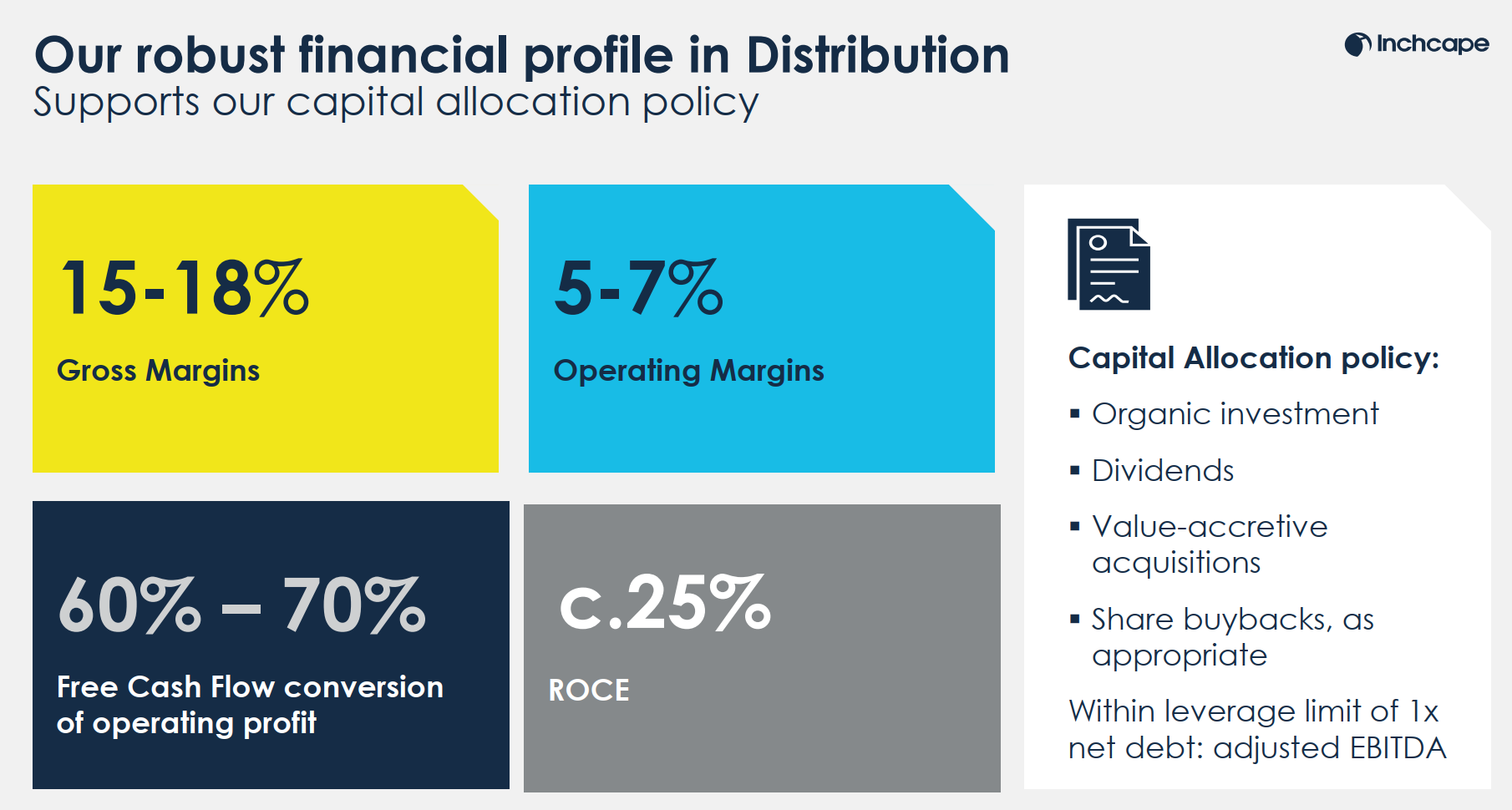

Inchcape management did a webinar titled "In the Driving Seat: Our Distribution Model", focusing on their distribution model, projected margins, FCF and ROCE.

III. General Themes & Thoughts

While Boeing and Airbus' full order books might seem to position them as obvious investment choices, it's actually the aircraft leasing companies that are benefiting most from the aircraft supply issues. AER 0.00%↑ CEO has consistently emphasized that Boeing and Airbus can’t produce the airplanes that they promised to make.

New flywheel just dropped:

IV. Closing Thoughts

I’m happy with the portfolio performance in the first half of the year, and excited about its prospects. They say slow and steady wins the race, but having potential fireworks through a catalyst is always fun. Both TIGO 0.00%↑ & CZR 0.00%↑ could see some of that in Q3.

If you enjoyed this post, please press a random button below.

FDEV has its roots in a profitable niche: CMS games (Creative Management Simulation) such as Planet Zoo, Planet Coaster and Jurassic World

Hello, thanks for sharing your portfolio and I appreciate your posts. As a fellow $FRFHF shareholder, curious when you got into Fairfax Financial and what your thoughts are at current price?